Open Now: The Global ETF Survey Take the Survey →

What Happens if You Buy and Hold a Leveraged ETF?

Daily reset leveraged ETFs are intended for short-term traders, but what does the data say about investing in them long-term as part of a buy-and-hold strategy?

Keep up with what matters in ETFs

Get timely ETF insights, market trends, and top ideas straight to your inbox.

Your newsletter subscriptions with us are subject to ETF Central's Privacy Policy and Terms and Conditions.

Back in February, I wrote about a niche subset of leveraged ETFs that are explicitly designed for long-term, buy-and-hold investors.

Those strategies typically use derivatives like futures and swaps not to deliver two or three times the daily return of a benchmark, but instead to apply modest leverage across diversified portfolios of relatively uncorrelated assets in an attempt to improve long-term risk-adjusted returns.

That’s very different from the leveraged ETFs most investors are familiar with. The typical leveraged ETF is designed to deliver two or three times the daily return of an underlying benchmark, whether that’s the S&P 500, Nasdaq 100, Russell 2000, a sector index, or increasingly, individual high-volatility stocks.

Providers like ProShares and Direxion are very explicit about this in their prospectuses, marketing materials, and fact sheets. These products are generally not intended to be long-term buy-and-hold investments, and over periods longer than a day, investor returns can diverge significantly from the stated leverage target.

That warning exists for a reason. Daily resetting leverage introduces path dependency. The sequence of returns matters just as much as the direction. In volatile markets, especially those that chop sideways, compounding effects can create what’s commonly referred to as volatility drag.

That can cause leveraged ETFs to underperform what investors might naively expect from simply multiplying long-term benchmark returns by two or three.

Still, despite those warnings, leveraged ETFs remain extremely popular, especially among retail investors. Some hold them tactically for a few days around catalysts. Others hold them for months or even years, betting that strong upward trends can overwhelm the effects of volatility drag.

So, what actually happens if you ignore the warnings and buy and hold them long term? That’s what we’re going to look at here. We’ll break down why leveraged ETF returns behave differently over time, then use historical back tests to examine what would have happened if investors had simply held some of the most popular leveraged ETFs over long periods.

Like what you're reading?

Stay in the loop — get the latest ETF insights: trends, analysis, and expert picks.

Why leveraged ETFs may behave differently long term

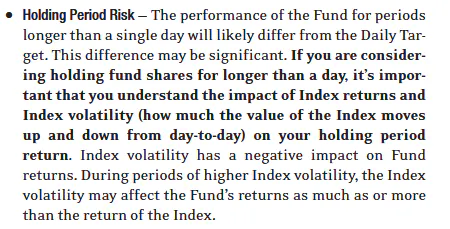

Right off the bat, I want to make one thing clear. The biggest risk with leveraged ETFs is not necessarily volatility drag. It’s the possibility of catastrophic capital loss.

If you hold a daily leveraged ETF targeting two times the return of an index, then mathematically, a 50% decline in the underlying benchmark in a single session would effectively wipe out your investment.

The odds of that happening depend heavily on what the ETF tracks. For something broad like the S&P 500, a 50% intraday collapse would be an extremely remote event. We’re talking about a true tail-risk scenario. In practice, market-wide circuit breakers would likely halt trading long before that happened.

But the further down the specialization ladder you go, the more realistic these risks become. Sector ETFs can move far more violently than broad indices, and single-stock leveraged ETFs are even riskier, especially for high-beta names around earnings announcements.

One way to think about that risk is through value at risk, or VaR. A 1% daily VaR estimates the loss threshold that historically would only be exceeded 1% of the time, while a 5% VaR does the same for more common downside scenarios. Conditional value at risk goes a step further. Instead of asking where the tail begins, it asks how bad losses historically became once that threshold was breached.

ETF providers calculate these kinds of statistics as part of their internal risk management frameworks before bringing leveraged products to market. Now, with the existential risk discussion out of the way, we can talk about holding period effects.

If you look at the prospectus for the ProShares UltraPro QQQ

Source: ProShares

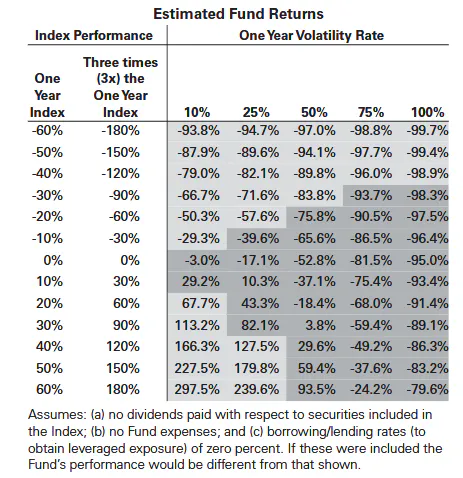

That warning matters because leveraged ETFs reset daily. All else being equal, the more volatile the underlying benchmark, the larger the divergence between the leveraged ETF’s return and simply multiplying the benchmark’s long-term return by two or three.

ProShares actually includes a helpful table showing different combinations of annual returns and volatility assumptions. What it demonstrates is straightforward: higher volatility generally produces worse outcomes for leveraged funds.

Source: ProShares

The easiest way to visualize this is with a simple example. Suppose an index rises 10% one day, then falls 10% the next. You might assume you’re back where you started, but you’re not. A 10% gain takes $100 to $110. A 10% decline on $110 then takes you down to $99. You lost money despite the index ending flat.

Leverage amplifies this effect because the daily reset compounds gains and losses asymmetrically. Add more volatility, especially sideways volatility, and the drag becomes increasingly severe over time. This is what I meant by “path dependant.”

Then there are the fees. Leveraged ETFs rely heavily on swaps to maintain exposure, which raises costs considerably compared to plain index funds. TQQQ, for example, carries a 0.95% expense ratio. That fee drag compounds over long holding periods as well.

In theory, all of this should make leveraged ETFs fairly unattractive as buy-and-hold investments. In practice, though, at least in the case of TQQQ, the historical results have been far more complicated than the warnings would suggest.

What actually happened with TQQQ long term?

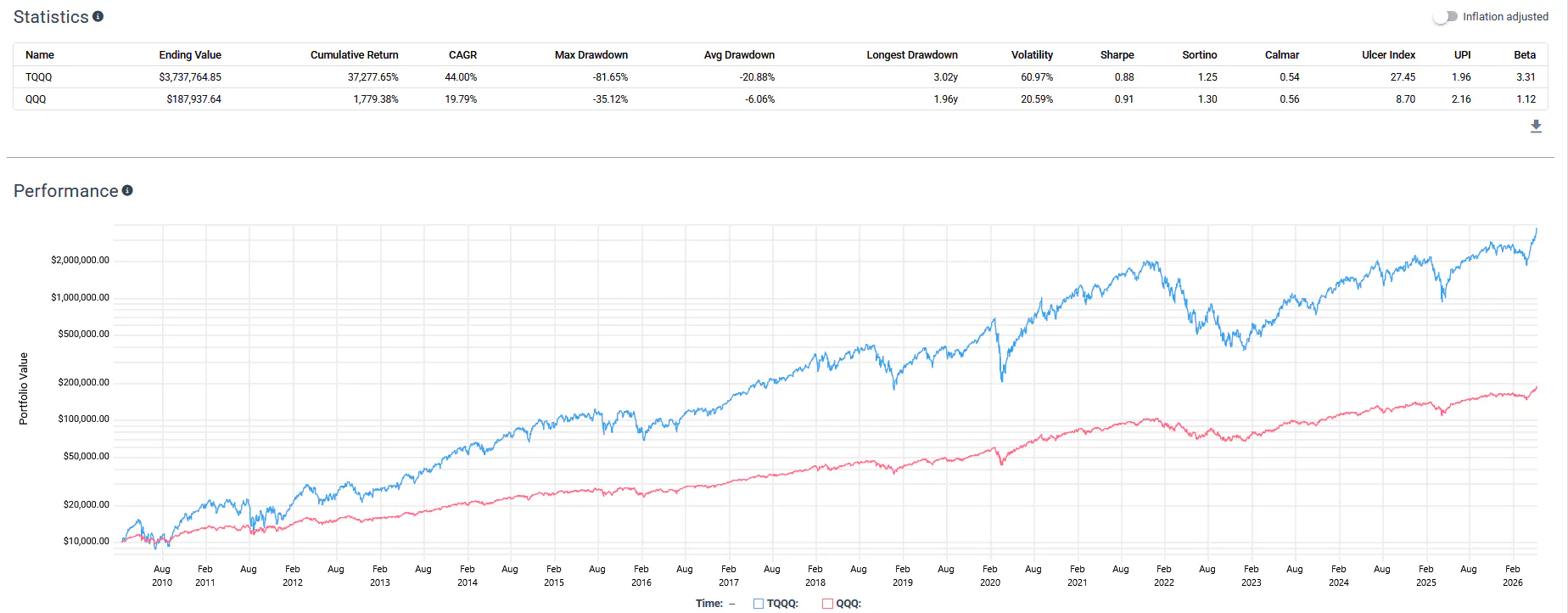

The obvious case study here is TQQQ which has been around long enough for us to meaningfully evaluate it against its unleveraged counterpart, Invesco QQQ Trust

Using a back test spanning roughly 16.24 years from February 11, 2010, through May 11, 2026, one thing becomes apparent immediately. TQQQ did not deliver exactly three times the long-term annualized return of QQQ. QQQ compounded at 19.79% annually, while TQQQ compounded at 44%.

Source: testfolio.io

That’s obviously far higher, but not a perfect 3x multiple. And that makes sense once you understand how leveraged ETFs work. On a day-to-day basis, the leverage target is generally very close. But as you extend the holding period into weeks, months, and years, compounding effects take over. Returns build on prior returns, and the path of volatility begins to matter more than the simple arithmetic.

Still, while annualized returns fell short of a literal 3x multiple, cumulative returns were absurdly strong. An investor buying and holding QQQ over the period, reinvesting distributions and ignoring taxes, would have earned roughly 1,779.38% cumulatively. TQQQ, meanwhile, delivered about 37,277.65%.

That result looks shocking until you zoom out and consider the environment. This back test largely covers the aftermath of the 2008 financial crisis, a period characterized by low interest rates, strong technology leadership, and relatively contained volatility outside of episodes like 2018, 2020, and 2022. Those are almost ideal conditions for a leveraged growth product.

The risk metrics are interesting too. QQQ experienced a maximum drawdown of 35.12%. If leverage worked perfectly over the entire holding period, you might expect TQQQ to have suffered something closer to three times that loss. Instead, the maximum drawdown came in around 81.6%. Still catastrophic, obviously, but notably less than a simple 3x extrapolation.

The catch is that very few investors could realistically stomach an 81% drawdown lasting years. Most retail investors would likely capitulate. Most advisors would reject the strategy outright from a suitability standpoint.

Volatility, however, did scale much closer to expectations. QQQ posted annualized volatility of 20.59%, while TQQQ came in at 60.97%, almost exactly triple. Interestingly, risk-adjusted returns were not dramatically worse. TQQQ achieved a Sharpe ratio of 0.88 versus 0.91 for QQQ.

My takeaway here is that leveraged ETFs can function surprisingly well as long-term holdings under the right market conditions. Specifically, you want strong momentum, relatively low volatility, and a favorable macroeconomic backdrop. TQQQ benefited from one of the greatest large-cap technology bull markets in history.

That’s why I think some of the social media narratives around leveraged ETFs “always decaying to zero” are too simplistic. The outcome is entirely dependent on the underlying asset and the volatility regime. To illustrate that, look at the opposite example: the Direxion Daily 20+ Year Treasury Bull 3X Shares

Long-duration Treasurys have been stuck in a brutal environment for years. Rising rates, elevated volatility in the yield curve, and the financing costs associated with maintaining leveraged exposure have all worked against TMF holders.

From April 16, 2009, through May 11, 2026, TLT compounded at roughly 1.9% annually and produced a cumulative return of about 37.8%. Not great, but at least positive. TMF, meanwhile, compounded at negative 6.05% annually. Investors would have lost roughly 65.5% cumulatively, even after enduring reverse splits along the way.

Source: testfolio.io

In that case, volatility drag absolutely did what critics warn about. Drawdowns and volatility scaled up dramatically, but returns did not.

So, if you are going to hold leveraged ETFs long term (and I do not recommend that approach), the most important thing is understanding the underlying asset and the environment surrounding it.

Generally speaking, leveraged ETFs work best when the underlying experiences strong momentum, relatively low volatility, and supportive macro conditions. For TQQQ, that combination existed, but for TMF, it absolutely did not. As always, buyer beware.

Please note this article is for information purposes only and does not in any way constitute investment advice. It is essential that you seek advice from a registered financial professional prior to making any investment decision.

Mentioned ETFs

Further reading

Latest ETF News

See all ETF newsHow Investors can Maximize Tax Efficiency with Income ETFs

Trump Accounts: Here's Which ETFs You Can Invest In

The Two Best Types of Fixed-Income ETFs For Managing Cash

ETF Comparison: Roundhill Generative AI & Technology ETF Versus iShares A.I. Innovation and Tech Active ETF

Advantages of ETFs over Mutual Funds1/6

Advantages of ETFs over Mutual Funds1/6

Lower Costs

In this guide, we'll explore the advantages of ETFs over mutual funds, giving you valuable insights into why ETFs have gained significant popularity among investors like yourself.

Leveraged ETFs: Unlocking the Potential for Amplified Returns1/6

Understanding Leveraged ETFs

Explore leveraged ETFs: potential for amplified returns & risks. 5 ETFs to consider across equities, commodities & fixed income.

What is a Leveraged ETF?1/6

Introducing Leveraged and Inverse ETFs

In this guide, we'll dive into the world of leveraged ETFs, exploring their definition, mechanics, potential risks, and rewards.

Recent educational content

ETF Trends

ETF Industry KPIs July 20, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

ETF Trends

ETF Industry KPIs July 13, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

First Look ETF

First Look ETF: Cash Deployment, Bond, and Hedged ETFs

In this season 6 episode of First Look ETF, Stephanie Stanton examines the latest ETF marketplace trends with NYSE and guests.

ETF Trends

ETF Industry KPIs July 6, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

Browse all educational columns

Expert-Built ETF Portfolios, All in One Place

Don’t start from scratch. Discover ready-made ETF portfolios built by professionals to match different goals, timelines, and market views. Use them as inspiration or as a starting point for your own allocation.