Open Now: The Global ETF Survey Take the Survey →

The Harry Browne permanent ETF portfolio

Harry Browne favours this simple yet diversified portfolio. Let's break it down.

Keep up with what matters in ETFs

Get timely ETF insights, market trends, and top ideas straight to your inbox.

Your newsletter subscriptions with us are subject to ETF Central's Privacy Policy and Terms and Conditions.

Back in 2001, American writer, politician, and investment advisor Harry Browne laid out the groundwork for his "Permanent Portfolio" in his book Fail-Safe Investing. Browne intended this portfolio to be a one-size-fits-all, permanent holding suitable for investors of all ages and risk tolerances.

The point of the permanent portfolio was to create an investment that could withstand most market conditions while still delivering solid returns, thus saving investors the need to time the market or pick which assets would outperform.

Like what you're reading?

Stay in the loop — get the latest ETF insights: trends, analysis, and expert picks.

How does the permanent portfolio work?

The permanent portfolio is an excellent illustration of the benefits of diversification. Simply put, a portfolio of volatile, uncorrelated assets with positive expected returns can produce more units of return for fewer units of risk compared to a single asset. This is why a 60/40 portfolio of stocks/bonds has a historically better Sharpe ratio than the S&P 500.

Diversification aims to produce the best risk-adjusted return, not maximize absolute returns. Ideally, the more volatility and drawdowns we risk, the more returns we should be compensated with. Spreading our sources of risk out among different assets with varying degrees of correlation to each other helps achieve this.

Brown outlined four different asset classes that were expected to outperform based on his theory of economic scenarios:

- Economic expansion: U.S. stocks.

- Economic deflation: U.S. long-term Treasury bonds.

- Economic recession: Cash & money market instruments.

- Economic inflation: Gold bullion.

The role of stocks

Stocks will drive most of the portfolio's returns during bull markets. Browne suggested using the total U.S. stock market, which saves investors the trouble of picking stocks. The S&P 500 could work, but in this case, maximizing diversification by including mid and small-cap stocks is probably a good idea.

The following low-cost index ETFs could work:

The role of bonds

Bonds (Treasurys) provide deflationary crash protection. When a market crash occurs, central banks often drop interest rates to stimulate the economy, which sends bond prices (especially long-term Treasurys) soaring. This is called the "flight to safety." Bonds also generally lower volatility (in a non-rising rate environment). Browne favoured long-term Treasurys, which provide the highest sensitivity to interest changes.

The following low-cost index ETFs could work:

The role of gold

Gold's inflation protection is debatable. Over the long term (think 50+ years), gold acts as a value store. In the short term, gold is too volatile and can easily tank when inflation soars due to other variables. I conceded that it acts as a safe haven for political/socio-economic turmoil and has a low correlation with stocks and bonds, making it a valuable diversifier.

The following low-cost index ETFs could work:

The role of cash

When all else fails, cash is king. Despite losing value to inflation, cash is unaffected by market crashes, giving investors some respite when the rest of their portfolio draws down. Now Browne didn't advocate for stuffing cash under your mattress. Instead, he suggested money market instruments like ultra short-term Treasury bills (T-Bills).

The following low-cost index ETFs could work:

Constructing the portfolio

Browne suggested the following equal weight allocation:

- 25% stocks

- 25% long-term Treasurys

- 25% gold

- 25% cash

These allocations are not mean-variance optimized or accurate for a true risk parity weighting. Browne's weights were intended to be a helpful rule of thumb for investors that could be easy to implement. I would also be cautious of using backtests to find the "correct" allocations as that is highly subject to over-fitting data.

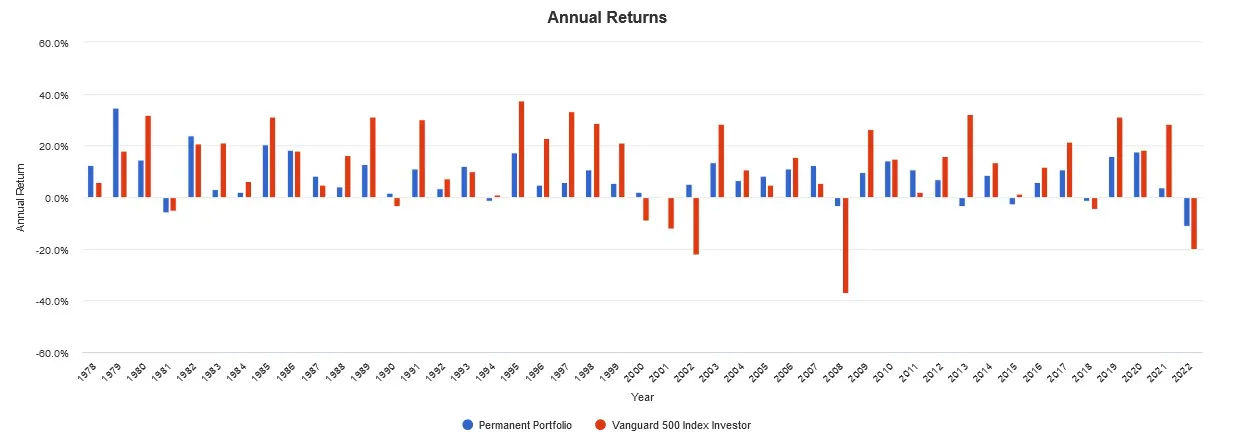

That being said, here's how it has performed compared to the S&P 500 since 1978 with annual rebalancing:

We see slightly better risk-adjusted returns (Sharpe ratio) but significantly lower volatility and drawdowns. Overall, the sequence of returns was much more predictable, which can be desirable for low-risk investors.

Personally, I would prefer a lower allocation to gold and cash (10% each) and replace some of the long-term Treasurys with intermediate duration ones. I would also swap out the U.S. stock market with the total world stock market. Then again, who am I to argue against Harry Browne?

Latest ETF News

See all ETF newsCan Gold Miner ETFs Be a Better Alternative to Leveraged Gold ETFs?

Options-Based ETFs as Fixed-Income Alternatives: What Investors Should Know

Avoid S&P 500 Concentration Risk with These Two ETFs

How Investors can Maximize Tax Efficiency with Income ETFs

Advantages of ETFs over Mutual Funds1/6

Advantages of ETFs over Mutual Funds1/6

Lower Costs

In this guide, we'll explore the advantages of ETFs over mutual funds, giving you valuable insights into why ETFs have gained significant popularity among investors like yourself.

Leveraged ETFs: Unlocking the Potential for Amplified Returns1/6

Understanding Leveraged ETFs

Explore leveraged ETFs: potential for amplified returns & risks. 5 ETFs to consider across equities, commodities & fixed income.

What is a Leveraged ETF?1/6

Introducing Leveraged and Inverse ETFs

In this guide, we'll dive into the world of leveraged ETFs, exploring their definition, mechanics, potential risks, and rewards.

Recent educational content

ETF Trends

ETF Industry KPIs July 20, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

ETF Trends

ETF Industry KPIs July 13, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

First Look ETF

First Look ETF: Cash Deployment, Bond, and Hedged ETFs

In this season 6 episode of First Look ETF, Stephanie Stanton examines the latest ETF marketplace trends with NYSE and guests.

ETF Trends

ETF Industry KPIs July 6, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

Browse all educational columns

The ETF Industry Is Evolving Fast

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.