Open Now: The Global ETF Survey Take the Survey →

Long Volatility ETFs: Use cases & risks

Going long volatility with VIX futures funds often turns into a market-timing exercise.

Keep up with what matters in ETFs

Get timely ETF insights, market trends, and top ideas straight to your inbox.

Your newsletter subscriptions with us are subject to ETF Central's Privacy Policy and Terms and Conditions.

Earlier, I wrote about the 2018 "Volmageddon" debacle, where numerous short-volatility exchange-traded products (ETPs) blew up in spectacular fashion. If you're not familiar with the incident, consider giving it a read, the story is as funny as it gets.

Volmageddon asides, the normal retail use for volatility products isn't shorting but rather as a sort of hedge. Unfortunately, going through long volatility is a bit of a timing exercise that has burned many an unsuspecting investor.

From contango, mean reversion, and high fees – there's no shortage of ways investors have lost money using long volatility instruments. Let's look into it further.

The ETF Industry Is Evolving Fast

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.

What is volatility?

When we say "long volatility," we're talking about betting on the value of the Chicago Board of Options Exchange (CBOE) Volatility Index (VIX) to go up. This index is calculated using the market's expectations of implied volatility based on SPX index options (calls and puts). If options traders think the market is likely to experience sudden movements, they buy more options, and thus the VIX moves.

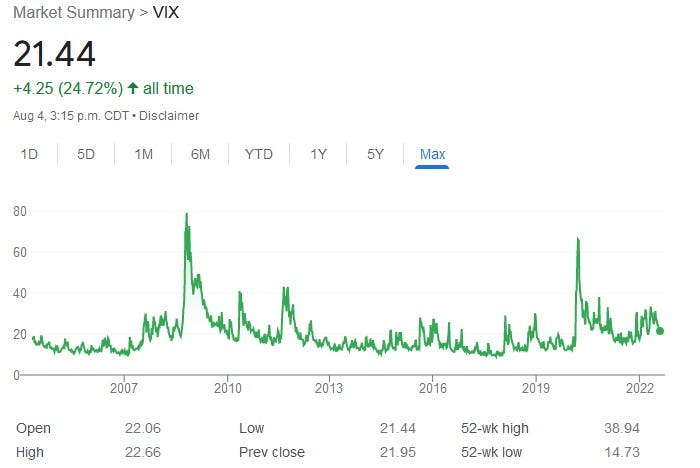

It's important to note that the VIX does not measure the actual volatility of the markets. It only measures a trader's expectations of volatility. Usually, those are fairly similar, but they can diverge accordingly if traders over or under-react. Generally, though, it’s a fairly accurate estimate. Take a look at the chart below and notice how the VIX spiked during numerous notable market crashes.

Going long volatility

Many investors will quickly realize that if the VIX tends to spike during market crashes, then perhaps it could be a reliable and effective hedge. Well, only the former is true. The VIX isn’t a reliable hedge because investors cannot buy it directly.

Instead, investors can only access the VIX through futures contracts, which are derivatives that bet on the future anticipated value of the VIX. A futures contract is an agreement to deliver something at a certain point in the future for a price that's agreed upon in the present. VIX futures are settled in cash depending on the results upon expiration.

The problem with futures contracts is contango, a fancy concept that destroys value rather quickly. Contango occurs in VIX futures when the price for a later-dated contract is higher than its current price. For example, if the VIX is trading at 20 today, but a one-month expiry VIX futures contract is at 22, then the VIX futures market is in contango.

The loss comes from what is called negative roll yield. Investors going long with VIX futures must constantly sell expiring ones for cheap and simultaneously buy later dated ones at a higher price. This is literally "buy high, sell low," which quickly erodes value over time.

Even without contango, the VIX is mean reverting. Over long periods of time, the VIX usually settles back to an average. Low-volatility bull markets are far more common than high-volatility bear markets. This is not ideal to bet against if you are long volatility – after all, your investment only increases in value if volatility does. If it constantly falls back to an established level, then you're constantly losing money.

ETF Example: VIX futures ETFs

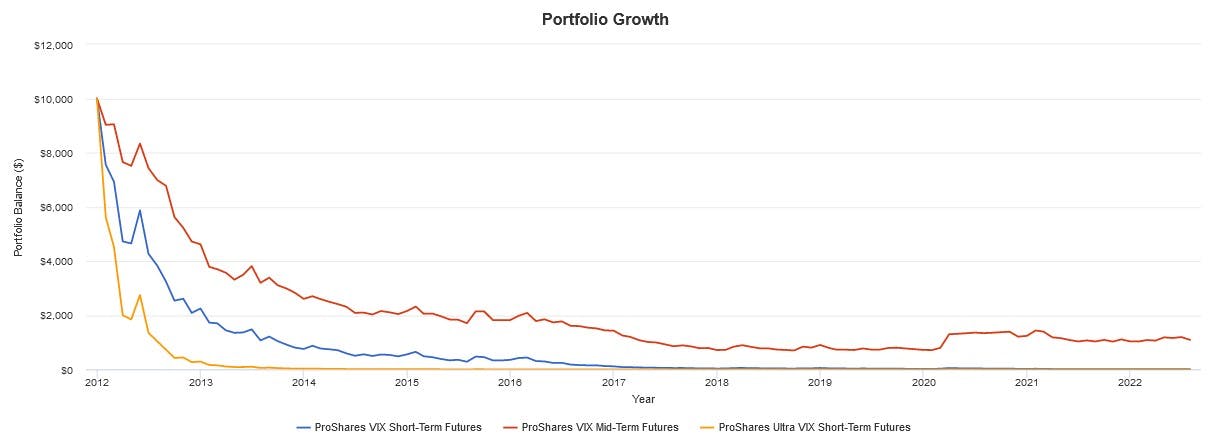

Due to contango, long VIX futures ETFs suffer from extreme price decays and mathematically trend towards zero. These ETFs rely on frequent reverse splits to maintain their share price and constant inflows of investor capital to ensure assets under management (AUM) stay sufficient.

For example, consider the following three long VIX futures ETFs below and their historical performance:

- ProShares VIX Short-Term Futures ETF (VIXY): 0.85% expense ratio.

- ProShares VIX Mid-Term Futures ETF (VIXM): 0.85% expense ratio.

- ProShares Ultra VIX Short-Term Futures ETF (UVXY): 0.95% expense ratio.

We can note several things:

- VIXM suffers less from decay compared to VIXY due to its use of further-dated VIX futures, which minimizes the effects of contango. However, this means it can track the VIX less accurately (short-term futures are more accurate), as seen by its more muted movements.

- UVXY decays horrendously fast as it is essentially a 1.5x daily leveraged version of VIXY. Even during high-volatility years like 2020, UVXY still underperforms VIXY on periods longer than a day due to how high volatility negatively affects the geometric mean.

- All three assets had a very high negative correlation with the S&P 500 of -0.80, -0.69, and -0.76, respectively, making them effective crash protection if you can time it right.

The use cases for long VIX ETFs are strictly tactical. If you have a reliable method of forecasting a market crash, going long volatility for a short period could be an effective hedge. For longer periods, this method suffers from a strong negative carry due to contango and high fees, making other instruments like put options or long-term Treasurys more appropriate.

Latest ETF News

See all ETF newsMoneyShow Chart of the Day 7/16/26: Good News/Bad News on Inflation (and the Fed)

MoneyShow Chart of the Day 7/1/26: The H1 Scorecard – and What Comes Next

MoneyShow Chart of the Day 6/22/26: Are World Cup Videos Helping US Companies Clean Up?

MoneyShow Chart of the Day 6/3/26: AI. AI. AI. (And a Handful of Other Stocks, Too)

Advantages of ETFs over Mutual Funds1/6

Advantages of ETFs over Mutual Funds1/6

Lower Costs

In this guide, we'll explore the advantages of ETFs over mutual funds, giving you valuable insights into why ETFs have gained significant popularity among investors like yourself.

Leveraged ETFs: Unlocking the Potential for Amplified Returns1/6

Understanding Leveraged ETFs

Explore leveraged ETFs: potential for amplified returns & risks. 5 ETFs to consider across equities, commodities & fixed income.

What is a Leveraged ETF?1/6

Introducing Leveraged and Inverse ETFs

In this guide, we'll dive into the world of leveraged ETFs, exploring their definition, mechanics, potential risks, and rewards.

Recent educational content

ETF Trends

ETF Industry KPIs July 20, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

ETF Trends

ETF Industry KPIs July 13, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

First Look ETF

First Look ETF: Cash Deployment, Bond, and Hedged ETFs

In this season 6 episode of First Look ETF, Stephanie Stanton examines the latest ETF marketplace trends with NYSE and guests.

ETF Trends

ETF Industry KPIs July 6, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

Browse all educational columns

Expert-Built ETF Portfolios, All in One Place

Don’t start from scratch. Discover ready-made ETF portfolios built by professionals to match different goals, timelines, and market views. Use them as inspiration or as a starting point for your own allocation.