Open Now: The Global ETF Survey Take the Survey →

Tony's ETF Buyer's Guide: Hedging Against a Market Crash

Here are your ETF options when it comes to insurance against significant market downturns.

Keep up with what matters in ETFs

Get timely ETF insights, market trends, and top ideas straight to your inbox.

Your newsletter subscriptions with us are subject to ETF Central's Privacy Policy and Terms and Conditions.

The first week of August has left many equity investors shaken, challenging the previously unshaken belief that the "line only goes up."

The turmoil began during earnings week, as numerous mega-cap tech companies reported weaker-than-expected results. Given their significant weight in major market cap-weighted indexes like the S&P 500 and Nasdaq 100, these underperformances triggered a notable correction.

The situation was exacerbated when the Bank of Japan unexpectedly hiked rates on July 31st and announced plans to taper bond purchases, causing the yen to plummet and Japanese stocks to sell off massively during what would be overnight trading in the U.S.

By the market open on Monday, August 5th, the scene was set for chaos: the S&P 500 closed down 3%, and the VIX spiked from 23 to over 60, marking its third-highest reading since the COVID-19 outbreak in March 2020 and the 2008 financial crisis.

Personally, I recommend taking a broader perspective. Despite the recent drops, the S&P 500 was still up 11.61% in price return as of August 6th. Corrections are a natural and healthy part of investing in equities, so it's important to stay calm.

That said, if you're looking to prepare for the next significant market downturn—remember, as the saying goes, bears have predicted 15 out of the last 3 recessions—there are a few ETFs that can serve as financial insurance.

However, keep in mind that, like any insurance, these instruments are not a free lunch and are typically priced in favor of the house, not the investor.

The ETF Industry Is Evolving Fast

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.

Long volatility ETFs

You might think that investing directly in the VIX—the market's volatility index—would be a straightforward way to benefit from market crashes. However, it's not that simple.

You can't directly invest in the VIX itself, as it's an index that measures the market's expectation of volatility over the next 30 days, based on S&P 500 index options.

Instead, to gain exposure to the VIX, you must use derivatives—specifically, VIX futures. These futures contracts bet on the future price of the VIX, and yes, you can access these futures via ETFs. But there are a few critical points to understand.

Firstly, VIX futures are not a perfect replacement for the VIX itself—their prices are correlated to, but not synonymous with, the spot price of the VIX. Generally, shorter expiry futures track the spot price more closely, while longer-dated ones do so less accurately.

Another significant aspect to consider is the net asset value (NAV) of these ETFs, which tends to decay over time. This decay occurs primarily because the VIX futures curve is often in contango, meaning future prices are higher than the spot price, leading to losses when futures contracts are rolled over at higher prices.

Additionally, the VIX is mean reverting, which means that volatility spikes are generally temporary and tend to return to a median level over time. This dynamic causes long volatility ETFs to perform poorly over extended periods.

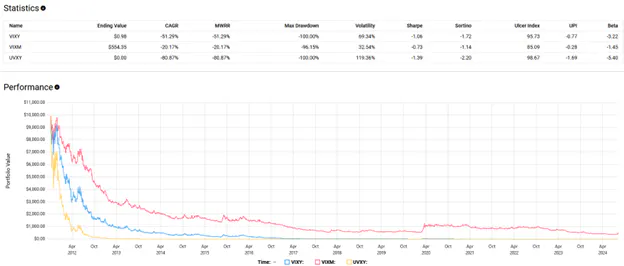

Three ETFs that provide exposure to VIX futures are the ProShares Ultra VIX Short-Term Futures ETF

VIXY and UVXY are the most correlated to the spot VIX, as they track short-term futures. UVXY is particularly notable because it is leveraged 3x, providing amplified exposure to changes in the VIX.

On the other hand, VIXM, which tracks mid-term futures, has less correlation to the spot VIX, but its NAV erodes more slowly due to its longer-dated futures.

Personally, I would not recommend using these ETFs because of the negative carry—the cost of holding these ETFs over time—and the fact that successfully capitalizing on them involves precise market timing.

You might incur gradual losses over time (more slowly for VIXM, more quickly for UVXY), waiting for a significant market crash that may or may not arrive. When a crash does happen, you must act quickly and accurately to rebalance or take profits at the right moment.

Tail risk ETFs

A bad market crash exemplifies tail risk—a high-severity, low-probability event that, assuming a normal distribution of outcomes, sits three standard deviations down on the left tail.

These are the kinds of events you truly want to hedge against. Not the gradual downturns like 2022, where trends emerge and you can adjust your strategy, but sudden, unexpected, and catastrophic losses that occur rarely.

Interestingly, there are ETFs specifically designed to hedge against these kinds of risks—tail risk ETFs. Most of these ETFs employ put options on major indexes to achieve their goal.

Unlike the long volatility ETFs, the negative carry—the cost of maintaining the hedge—is significantly less. You'll still pay to hold them, much like an insurance policy, but the premiums are less burdensome.

From Cambria ETFs, we have two examples: the Cambria Tail Risk ETF

Both ETFs maintain a core holding of Treasuries, which not only helps offset the cost of the puts but also provides additional diversification away from equity risk, albeit with the trade-off of interest rate risk in years like 2022.

These ETFs are also much cheaper than their long volatility counterparts, both charging a 0.59% expense ratio. While they do exhibit some negative carry, they have delivered what's known as "crisis alpha" during significant downturns, like in March 2020 during the onset of COVID-19 and more recently during the market downturn on August 5th.

Another intriguing option is the Alpha Architect Tail Risk ETF

I'm cautiously impressed with CAOS, which has delivered positive carry since its launch in March 2023. It hasn't yet been tested in a major crash, but it was in the green on August 5th. I'm curious to see how the box spread and put spread strategies perform when rates fall and during a major market crash.

Unlike the long volatility ETFs, these tail risk ETFs can be held long-term. The idea is to "diversify your diversifiers"—you layer on fixed income, trend-following, and then a small allocation to tail risk hedges like these ETFs.

Please note this article is for information purposes only and does not in any way constitute investment advice. It is essential that you seek advice from a registered financial professional prior to making any investment decision.

Topics

See all

Mentioned ETFs

Further reading

Latest ETF News

See all ETF newsAvoid S&P 500 Concentration Risk with These Two ETFs

How Investors can Maximize Tax Efficiency with Income ETFs

Trump Accounts: Here's Which ETFs You Can Invest In

The Two Best Types of Fixed-Income ETFs For Managing Cash

Advantages of ETFs over Mutual Funds1/6

Advantages of ETFs over Mutual Funds1/6

Lower Costs

In this guide, we'll explore the advantages of ETFs over mutual funds, giving you valuable insights into why ETFs have gained significant popularity among investors like yourself.

Leveraged ETFs: Unlocking the Potential for Amplified Returns1/6

Understanding Leveraged ETFs

Explore leveraged ETFs: potential for amplified returns & risks. 5 ETFs to consider across equities, commodities & fixed income.

What is a Leveraged ETF?1/6

Introducing Leveraged and Inverse ETFs

In this guide, we'll dive into the world of leveraged ETFs, exploring their definition, mechanics, potential risks, and rewards.

Recent educational content

ETF Trends

ETF Industry KPIs July 20, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

ETF Trends

ETF Industry KPIs July 13, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

First Look ETF

First Look ETF: Cash Deployment, Bond, and Hedged ETFs

In this season 6 episode of First Look ETF, Stephanie Stanton examines the latest ETF marketplace trends with NYSE and guests.

ETF Trends

ETF Industry KPIs July 6, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

Browse all educational columns

The ETF Industry Is Evolving Fast

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.