Open Now: The Global ETF Survey Take the Survey →

Tony’s ETF Buyer’s Guide: Hedged Equity ETFs

These alternative ETFs use sophisticated multi-leg option strategies to lower volatility and drawdowns, but come at the cost of capped upside and higher fees.

Keep up with what matters in ETFs

Get timely ETF insights, market trends, and top ideas straight to your inbox.

Your newsletter subscriptions with us are subject to ETF Central's Privacy Policy and Terms and Conditions.

Options-based ETFs have grown rapidly, and the results have been mixed. Some of the newer launches focus on single stocks with synthetic covered call exposure.

In practice, many of these products have delivered poor total returns relative to the underlying stocks once slippage, expense ratios, and taxes are considered. Monthly distributions often look attractive on the surface, but a large portion tends to be return of capital, meaning investors are receiving their own money back.

There is a more constructive side to this trend. A newer group of hedged equity ETFs has emerged that takes a different approach. These are not buffer ETFs tied to specific monthly or quarterly vintages, and they do not require precise timing. Instead, they are designed as evergreen strategies that continuously manage risk. In that sense, they function more like long-term portfolio components than tactical trades.

These strategies have gained attention because many investors and advisors are still reacting to periods when a traditional 60-40 portfolio experienced drawdowns close to those of an all-equity allocation. Rising inflation and higher interest rates reduced the diversification benefit of bonds, particularly for portfolios with meaningful duration exposure.

Hedged equity ETFs attempt to address that problem directly by using options to dampen equity volatility rather than relying on bonds for diversification. They are also becoming more affordable relative to older mutual fund equivalents, and they benefit from the tax efficiency of the ETF structure, including fewer or no year-end capital gains distributions.

To show how these ETFs work in practice, the sections that follow walk through two examples from Fidelity and Simplify, and then compare them with a traditional 60/40 approach.

Like what you're reading?

Stay in the loop — get the latest ETF insights: trends, analysis, and expert picks.

Two Ways to Hedge Equity Risk

The first ETF under review is the Simplify Hedged Equity ETF

That choice matters. Rather than building an active stock portfolio, the strategy relies on a well-established benchmark and focuses its complexity where it is intended, in the risk management layer.

That risk management layer takes the form of a put-spread collar on the S&P 500. HEQT begins by buying a put option that is 5% out of the money. This establishes downside protection once the index falls beyond that level. To help finance the cost, the fund sells a put that is 20% out of the money. This means that losses begin to reappear once the index falls beyond that threshold.

On top of that, HEQT sells an out-of-the-money call option, which caps upside participation but generates additional premium that helps fully offset the cost of the put structure.

The payoff profile looks very different from a fully long equity position. Compared with owning the index outright, gains are muted during strong rallies, modest drawdowns are softened, and very deep selloffs reintroduce downside exposure after mitigating some initial losses.

Importantly, this is not a one-off discreet hedge that expires and disappears. HEQT ladders these collars across three sequential months and applies them to 100% of the portfolio’s notional equity exposure, which helps smooth outcomes over time.

One practical advantage relative to buffer ETFs is that dividends are not sacrificed. The fund still posts a 0.79% 30-day SEC yield, and retaining dividend participation matters for long-term total return. Costs are also reasonable for an options-based strategy, with a net expense ratio of 0.43%.

A different expression of the same broad philosophy comes from the Fidelity Hedged Equity ETF

The managers target a market-cap profile similar to the S&P 500 and rely on quantitative inputs for active stock selection, with the stated goal of outperforming the benchmark. That introduces manager discretion and some opacity relative to HEQT’s index-based approach.

The second difference lies in how options are used. FHEQ does not employ a collar. Instead, it holds a ladder of S&P 500 put options with varying strikes and expirations extending well into the future. These puts provide convex protection during sharp market declines, but they also create a steady cost as many of them expire worthless in calm or rising markets.

To put it simply, HEQT aims for a smoother ride with clearly defined trade-offs. Upside is capped, downside protection works within a specified range, and outcomes are relatively predictable. FHEQ accepts more ongoing drag in exchange for the possibility of stronger protection during severe selloffs. Both reduce equity risk, but with different trade-offs.

How They Fared Versus a Traditional 60-40 Portfolio

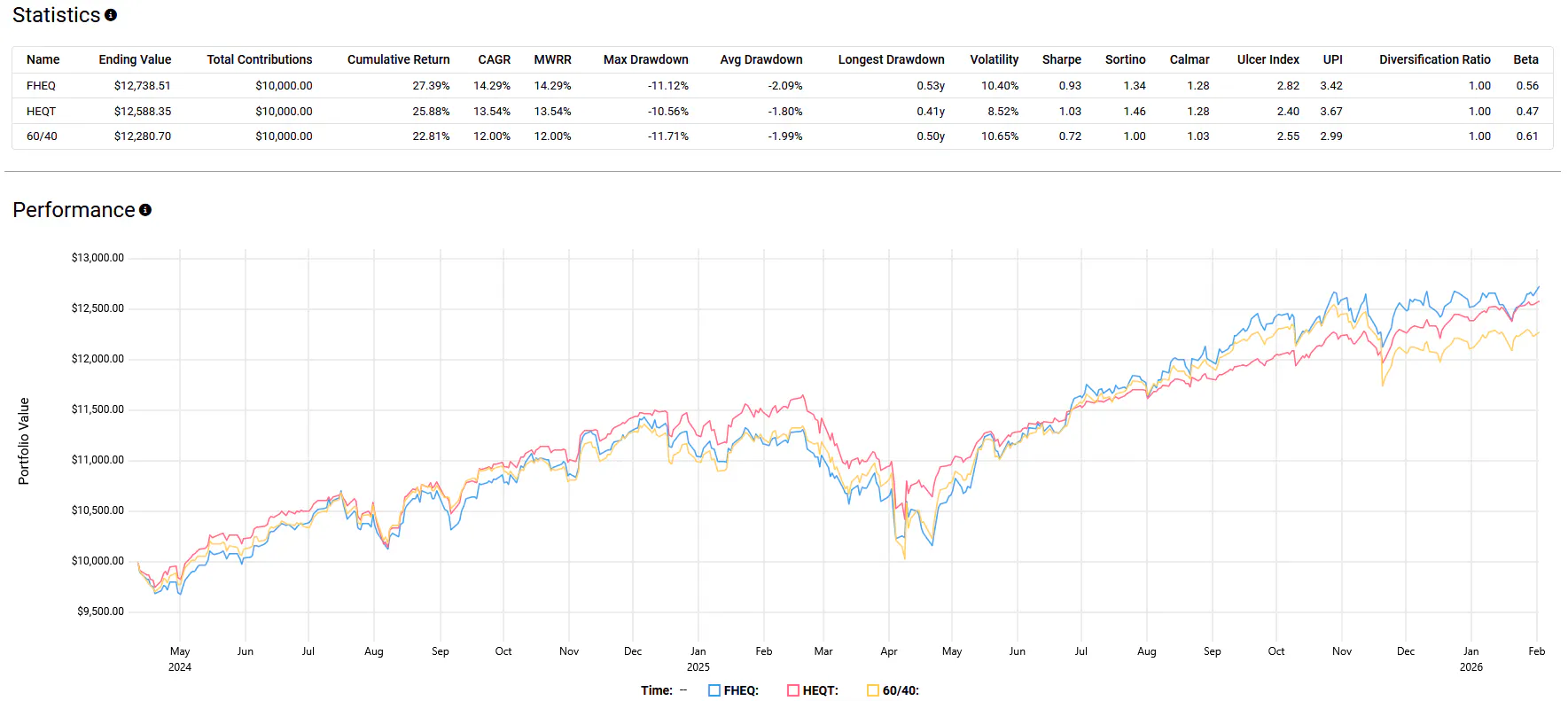

The shared performance window for these ETFs is short. The backtest covers roughly 1.81 years, from April 11, 2024, through February 2, 2026. That limits how much can be inferred, but the results so far are directionally consistent with what these strategies are designed to do.

Over this period, both ETFs outperformed the 60-40 on an absolute return basis. They also posted similar maximum drawdowns and comparable realized volatility. Where the difference shows up is in risk-adjusted performance. FHEQ recorded a Sharpe ratio of 0.93, HEQT came in at 1.03, and the 60-40 portfolio lagged at 0.72.

The gap between the two ETFs is also instructive. HEQT performed better on a risk-adjusted basis, which is not surprising given its collar structure that does better under modest to moderate volatility. FHEQ continues to experience ongoing theta drag as puts expire and new protection is purchased.

This period has not featured a sharp equity correction, so the convexity embedded in FHEQ’s option book has not had an opportunity to offset that drag. That protection is there if needed, but it has not been called upon yet. Conversely, drawdowns have also not been deep enough to breach the lower leg of HEQT’s put spread, where losses beyond roughly 20% would resume on a one-to-one basis.

This article is for informational purposes only and does not in any way constitute investment advice. The author may express their own opinions, which may not represent the opinions of ETF Central or its affiliated partners. It is essential that you seek advice from a registered financial professional prior to making any investment decisions.

Latest ETF News

See all ETF newsCrypto Income ETFs: Futures, Options, or Staking?

There’s an ETF for That? Air Conditioning Stocks

There's an ETF for That? Emerging Markets Without China

Autocallables Versus Equity-Linked Notes: Pros and Cons for Derivative Income ETFs

Advantages of ETFs over Mutual Funds1/6

Advantages of ETFs over Mutual Funds1/6

Lower Costs

In this guide, we'll explore the advantages of ETFs over mutual funds, giving you valuable insights into why ETFs have gained significant popularity among investors like yourself.

Leveraged ETFs: Unlocking the Potential for Amplified Returns1/6

Understanding Leveraged ETFs

Explore leveraged ETFs: potential for amplified returns & risks. 5 ETFs to consider across equities, commodities & fixed income.

What is a Leveraged ETF?1/6

Introducing Leveraged and Inverse ETFs

In this guide, we'll dive into the world of leveraged ETFs, exploring their definition, mechanics, potential risks, and rewards.

Recent educational content

ETF Trends

ETF Industry KPIs July 6, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

Asset TV

The ETF Show - The Evolution of Leveraged & Inverse ETFs

Leveraged and inverse ETFs have exploded in popularity over the past decade capturing more assets as retail traders seek to capture volatility.

Asset TV

The ETF Show - Investors Turn to Small Caps as Value Outperforms

After years of outflows, small caps have attracted interest as the Russell 2000 outperforms the broad market. Chris Parker, Senior Portfolio Manager from Thrivent Asset Management joins the ETF Show to discuss.

ETF Trends

ETF Industry KPIs 6/29/2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape:

Browse all educational columns

The ETF Industry Is Evolving Fast

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.