Open Now: The Global ETF Survey Take the Survey →

Meet the Biggest Winners of REIT Earnings Season - Q1 2026

A wave of guidance raises, improving fundamentals, and renewed deal activity revealed the REIT sectors gaining the most momentum in 2026.

Keep up with what matters in ETFs

Get timely ETF insights, market trends, and top ideas straight to your inbox.

Your newsletter subscriptions with us are subject to ETF Central's Privacy Policy and Terms and Conditions.

In Part 1 of our Earnings Recap, we highlight the Winners of REIT Earnings Season and the key takeaways from roughly 200 reports across equity REITs, mortgage REITs, and homebuilders over the past six weeks. In Part 2 later this week, we’ll turn to the laggards - including outright disappointments and in-line performers that failed to keep pace with the broader REIT rally.

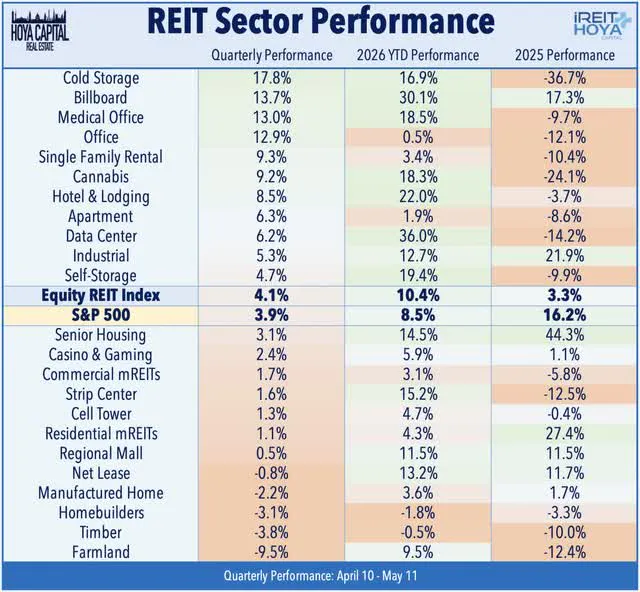

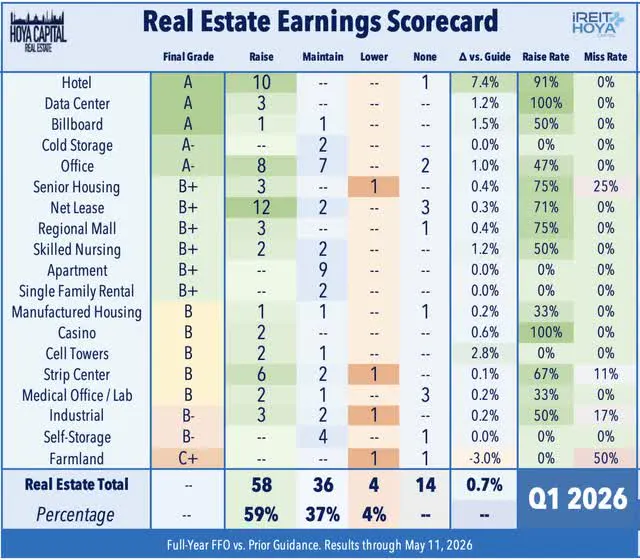

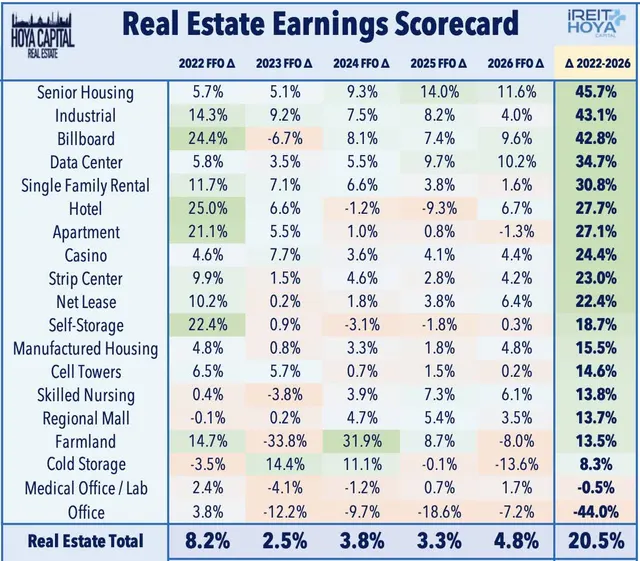

Over 200 U.S. REITs and homebuilders have reported first-quarter earnings results over the past six weeks, providing a critical update on the state of the commercial and residential real estate industry. Overall, REIT earnings results were considerably better than consensus expectations and delivered a notably cleaner reporting period than several recent quarters, with fewer high-profile disappointments and a broader mix of upside surprises across sectors and market-cap tiers. Of the 98 equity REITs that provided full-year FFO guidance, 58 REITs - or 59% - raised their outlooks, considerably above the typical first-quarter raise rate of roughly 40-45%, while 36 REITs - or 37% - maintained guidance, and just 4 REITs - or 4% - lowered guidance. Property-level trends were similarly solid, with same-store NOI guidance boosts coming from a balanced mix of expense controls and better-than-expected revenue trends, reflecting broad-based improvement across most major REIT property sectors. Since the start of earnings season, the Equity REIT Index is higher by 4.1%, outpacing the 3.9% gain from the S&P 500. The strong REIT earnings season is consistent with a better-than-expected reporting period across the broader U.S. equity market, where 84% of S&P 500 constituents have topped consensus EPS estimates, according to FactSet, above the five-year average.

The results have helped reframe the REIT narrative after several years in which higher rates, NAV discounts, and balance-sheet concerns dominated investor attention. Dividend activity also reinforced the improved tone, with dividend increases from SPG, CBL, CHCT, ADC, LINE, SKT, and CTRE, and a special dividend from HST.

Capital-market activity has improved, acquisition pipelines are reopening in sectors with attractive spreads, and several REITs used earnings season to highlight share repurchases, asset sales, deleveraging plans, and dividend increases.

The combination of stronger guidance trends, improving property fundamentals, and renewed deal activity has helped revive some long-dormant “animal spirits” across the sector, even as the broader macro backdrop remains far from ideal. Notable upside standouts this earnings season include Hotel, Senior Housing, Data Center, Billboard, Cold Storage, Net Lease, and Retail REITs.

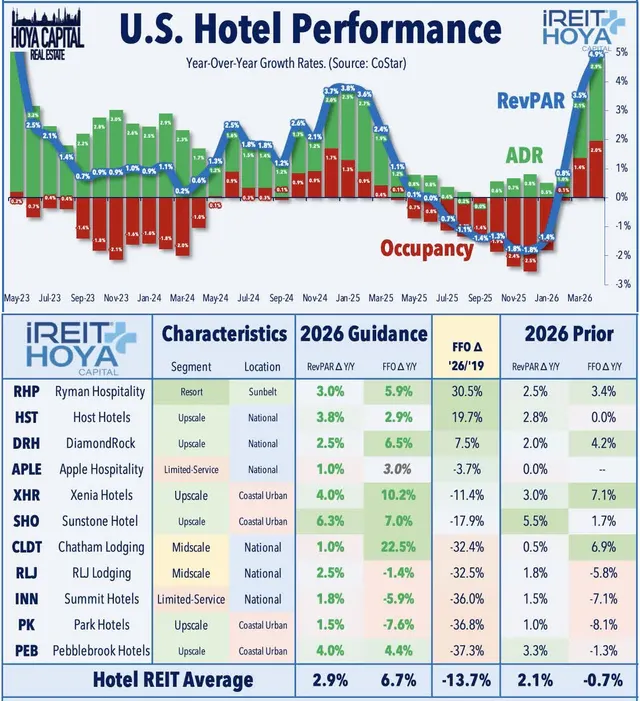

Hotel REITs delivered perhaps the cleanest upside surprise, with a perfect nine-for-nine slate of full-year FFO outlook raises, supported by resilient group travel, stronger urban demand, improving higher-end leisure trends, and solid margin control.

Billboard REITs showed no signs of cooling in local out-of-home advertising demand, while Cold Storage REITs halted their cold streak of misses with encouraging signs of stabilization after a difficult 2025. Office REITs reported the most constructive office earnings season in years, with eight REITs raising full-year FFO outlooks.

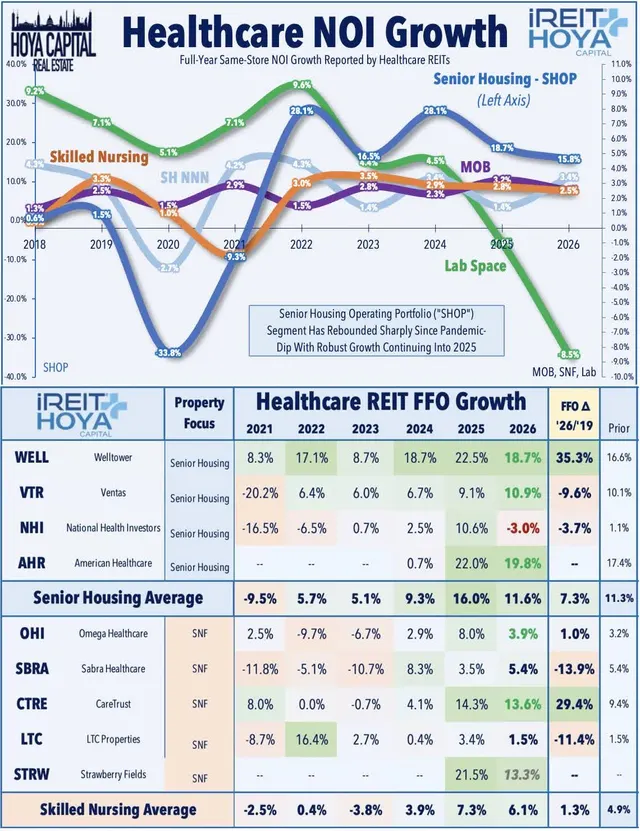

Elsewhere, Senior Housing REITs - again among the sector’s clear performance leaders - posted another stellar quarter, with continued SHOP outperformance and 2026 NOI growth expectations generally in the mid-to-high teens, driven by occupancy gains, limited new supply, and favorable demographic tailwinds.

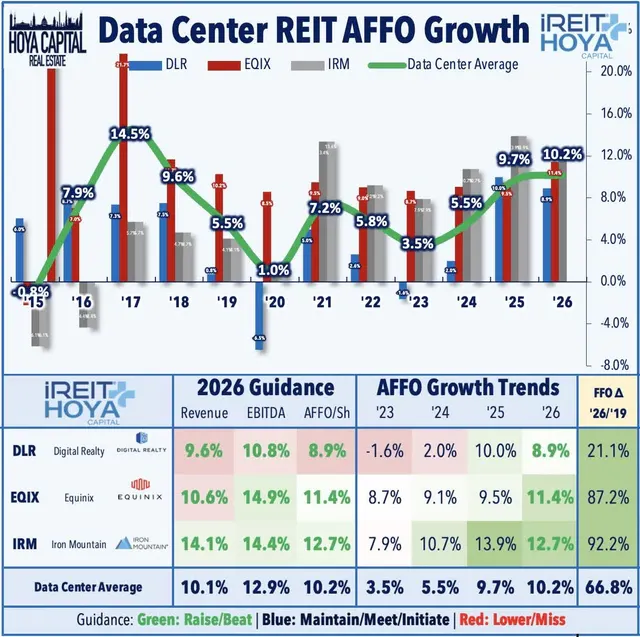

Data Center REITs continued to prove that they remain core infrastructure players in the AI boom, with leasing demand, vacancy, and pricing trends that still rival the strongest corners of the technology sector.

Net Lease REITs also turned in a strong season, with acquisition pipelines reaccelerating as cap rates remain attractive and external growth spreads continue to support guidance upside.

More broadly, results from Retail REITs - across strip center, regional mall, and outlet format - remained constructive, with limited new supply helping keep occupancy near record highs, rent spreads firmly positive, and several mall/outlet names raising dividends. Residential REITs - both Apartment and Single-Family Rental REITs - maintained guidance while reporting firmer April lease trends, suggesting that rent growth may be approaching a cyclical inflection as supply pressure begins to moderate.

Across the REIT sector, 32 REITs posted post-earnings gains of 10% or more, while three REITs gained more than 30%: Hudson Pacific (HPP), Industrial Logistics (ILPT), and Service Properties (SVC). Below, we discuss the sector-level Winners of REIT Earnings Season.

![]()

The ETF Industry Is Evolving Fast

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.

Winners of REIT Earnings Season

Winner #1: Hotel (Final Grade: A)

Positives: Perfect ten-for-ten slate of full-year FFO outlook raises; RevPAR guidance broadly lifted across the group; and Host declared a special dividend tied to gains from its Four Seasons asset sales. Strength was broad-based across select-service, resort, urban, and large-cap hotel platforms, supported by resilient group travel, higher-end leisure, improving business transient demand, special event calendars, and stronger-than-expected margin control.

Negatives: Macro sensitivity remains elevated if fuel prices, consumer caution, or corporate travel budgets weaken; some full-year FFO outlooks still imply modest declines despite guidance raises; recovery remains dependent on continued group demand, special events, and higher-end leisure resilience.

Big Winners: Chatham Lodging (CLDT), Summit Hotels (INN)

Winner #2: Data Center (Final Grade: A)

Positives: AI, cloud, and enterprise demand remain exceptionally strong, with robust leasing velocity, record or near-record backlogs, and sustained pricing power supporting premium valuations. DLR, EQIX, and IRM all showed durable demand trends, with development pipelines increasingly pre-leased and capital availability still supportive despite large expansion requirements.

Negatives: Valuations remain demanding relative to most REIT sectors; power availability, labor, supply-chain constraints, and development execution remain key bottlenecks; some quarterly results were affected by timing issues, while cash renewal spreads moderated modestly from peak levels.

Big Winners: Iron Mountain (IRM)

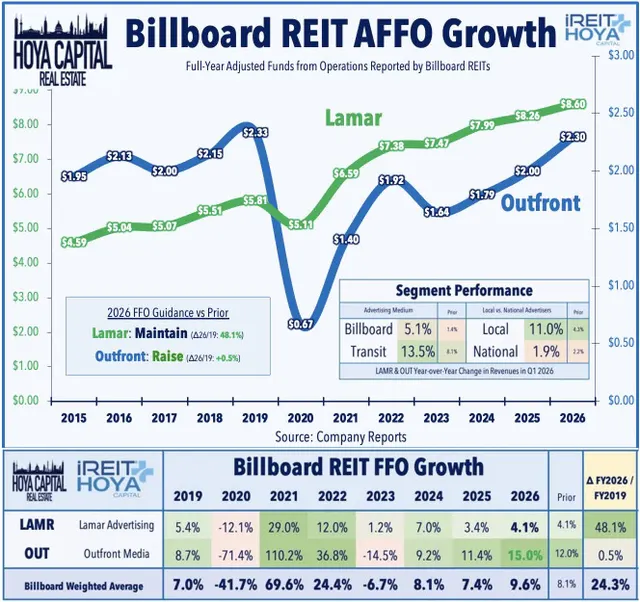

Winner #3: Billboard (Final Grade: A)

Positives: Stronger-than-expected out-of-home advertising demand across local, digital, programmatic, transit, airports, and logos. Lamar paced toward the high end or potentially above its guidance range, while Outfront raised its outlook as transit revenue, digital direct automated sales, and programmatic demand accelerated sharply from prior-year levels.

Negatives: National ad spending remained relatively weaker, averaging just +1.9% growth versus roughly +11% for local, suggesting some large advertisers remain cautious; advertising remains economically sensitive; political upside can be uneven and non-recurring; Outfront still carries balance-sheet and transit-exposure complexity.

Big Winners: Outfront (OUT), Lamar (LAMR)

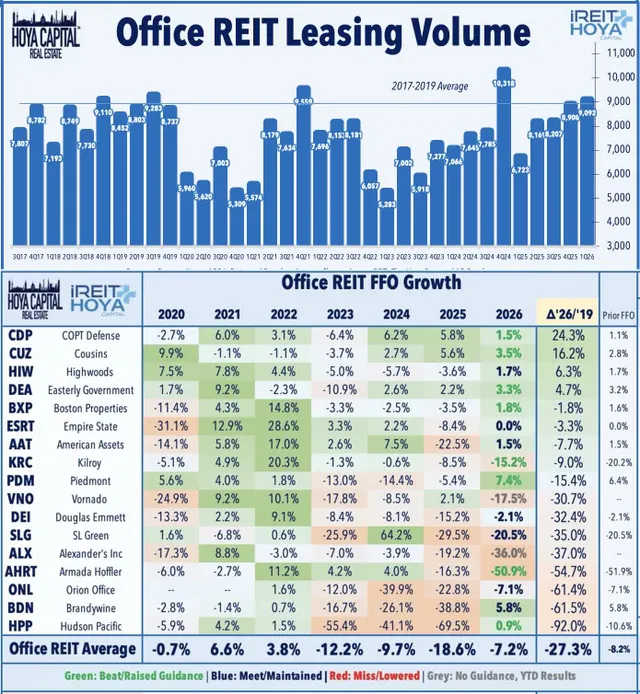

Winner #4: Office (Final Grade: A-)

Positives: Most constructive office earnings season in years, with eight REITs raising full-year FFO outlooks and none lowering guidance. Leasing activity, absorption, occupancy stabilization, and cash rent spreads all improved, with West Coast, NYC, Sunbelt, government/defense, and flight-to-quality portfolios showing better momentum than feared, reinforcing evidence that the sector’s cyclical trough is increasingly behind us.

Negatives: Recovery remains uneven and fragile, with occupancy still depressed and cash spreads negative across many markets; balance-sheet repair efforts are pushing the upward FFO inflection into 2027 despite better property-level trends; Mamdani’s property-tax threats have kept NYC-focused names under pressure despite solid NYC leasing trends.

Big Winners: Hudson Pacific (HPP), Douglas Emmett (DEI), Highwoods (HIW)

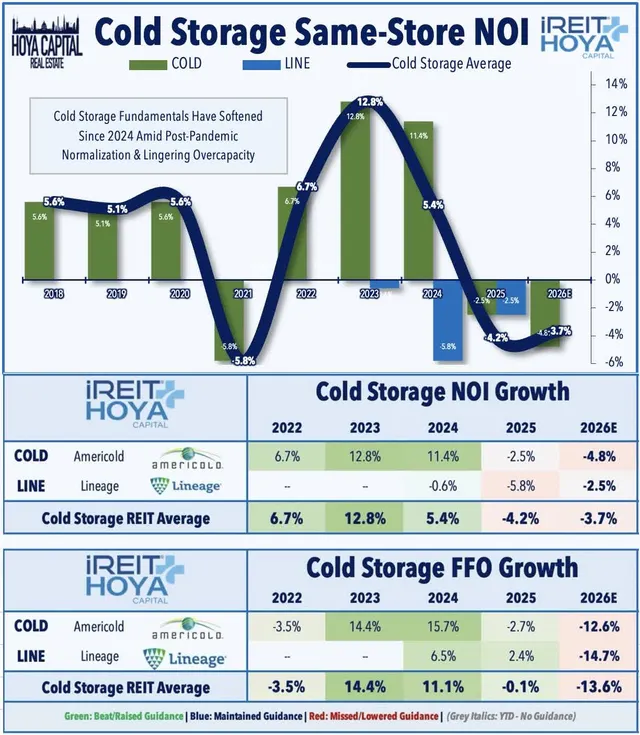

Winner #5: Cold Storage (Final Grade: A-)

Positives: Clear stabilization signs emerged after a difficult 2025, with Americold and Lineage both pointing to improving inventory, pricing, churn, and warehouse NOI trends. COLD’s EQT joint venture provides meaningful deleveraging proceeds, while LINE showed fourth-straight quarterly improvement in rent/storage revenue per pallet despite still-muted demand.

Negatives: Full-year outlooks still imply FFO and NOI declines, so this remains an early stabilization story rather than a full recovery. The sector remains exposed to elevated supply, post-COVID inventory normalization, trade-related throughput volatility, and balance-sheet repair needs, particularly after a sharp multi-year reset in fundamentals and investor confidence.

Big Winners: Americold (COLD), Lineage (LINE)

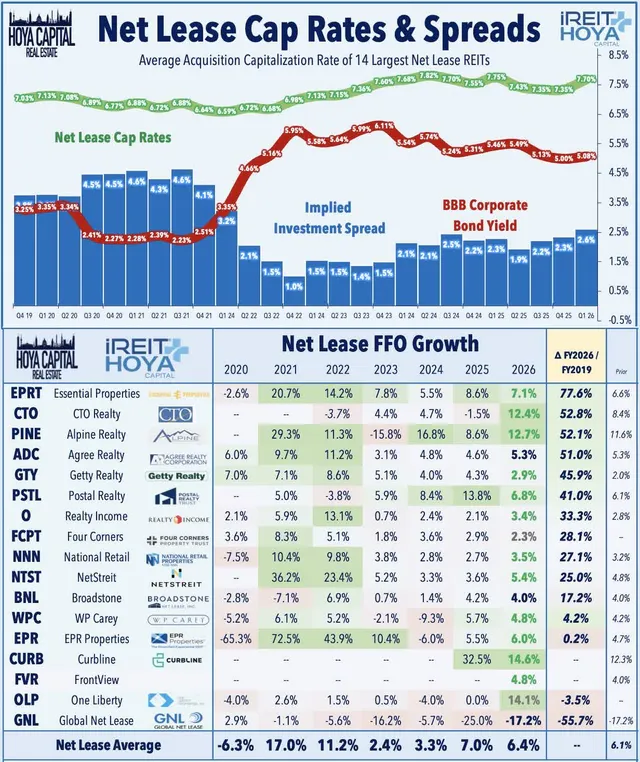

Winner #6: Net Lease (Final Grade: B+)

Positives: Solid earnings season, with 12 REITs raising full-year FFO outlooks as acquisition pipelines reaccelerated and external growth spreads remained attractive. Balance sheets remain broadly healthy, transaction activity is firm, cap rates appear stable, and both large-cap and small-cap names showed healthy investment volumes, occupancy, and rent recapture trends.

Negatives: Same-store growth remains modest, particularly for larger diversified names where external growth is required to drive meaningful upside. Equity issuance and capital raising capped stock reactions for several names, pockets of tenant softness emerged in casual dining and entertainment, and elevated rates keep cost-of-capital advantages concentrated among higher-quality platforms.

Big Winners: Postal Realty (PSTL), Modiv (MDV)

Big Losers: Global Net Lease (GNL), Essentials Property (EPRT)

Winner #7: Senior Housing (Final Grade: B+)

Positives: Senior housing remains the strongest property-level growth engine in REITs, with SHOP NOI growth often in the mid-to-high teens. Occupancy recovery, limited new supply, private-pay demand, and demographic tailwinds continue to support outsized growth, while external growth activity is broadening beyond WELL into AHR, VTR, and others.

Negatives: Growth remains concentrated in SHOP rather than non-SHOP healthcare segments; NHI lowered full-year FFO guidance due primarily to near-term dilution from its planned $560M NHC portfolio sale; Holiday SHOP assets and certain repositioning strategies remain uneven; valuation expectations are high after sustained sector outperformance.

Big Winners: Welltower (WELL)

Big Losers: National Health Investors (NHI)

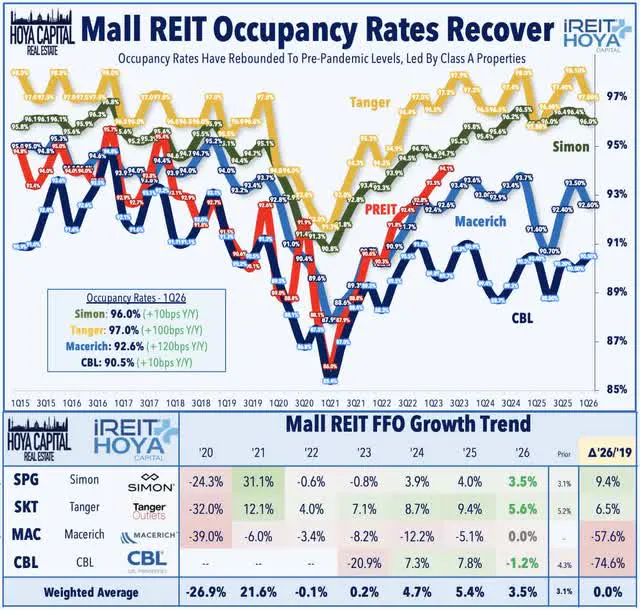

Winner #8: Regional Mall: (Final Grade: B+)

Positives: Mall and outlet REITs showed stronger core fundamentals, with Simon posting robust domestic NOI growth, accelerating tenant sales, higher base rents, resilient leasing demand, and a 96% leased rate. Tanger also showed healthy occupancy gains, solid leasing volumes, and positive tenant sales, while SPG, SKT, and CBL all raised dividends, reinforcing confidence in cash-flow durability.

Negatives: Simon’s headline FFO missed expectations due to stock comp and other items. Tanger’s beat was aided by lease termination fees, spreads compressed from 2025 levels, and sector confidence remains tied to affluent consumer resilience, redevelopment execution, and leasing momentum.

Big Winners: CBL Properties (CBL)

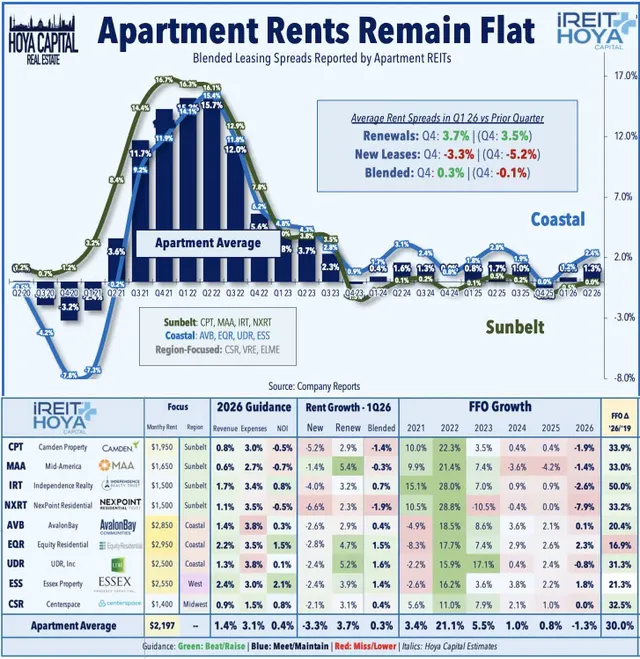

Winner #9: Apartment: (Final Grade: B+)

Positives: Apartment REITs maintained outlooks while April rent trends firmed, suggesting the sector is moving closer to a cyclical inflection. Coastal markets improved, Midwest fundamentals remained steady, and Sunbelt new lease pressure showed early signs of easing into peak leasing season as new supply begins to moderate.

Negatives: Full-year growth remains muted, with many outlooks calling for flat-to-negative FFO or low NOI growth. Sunbelt markets remain pressured by supply, concessions, and negative new lease spreads.

Big Winners: NexPoint Residential (NXRT), AvalonBay (AVB)

Big Losers: Elme Communities (ELME), Clipper Realty (CLPR)

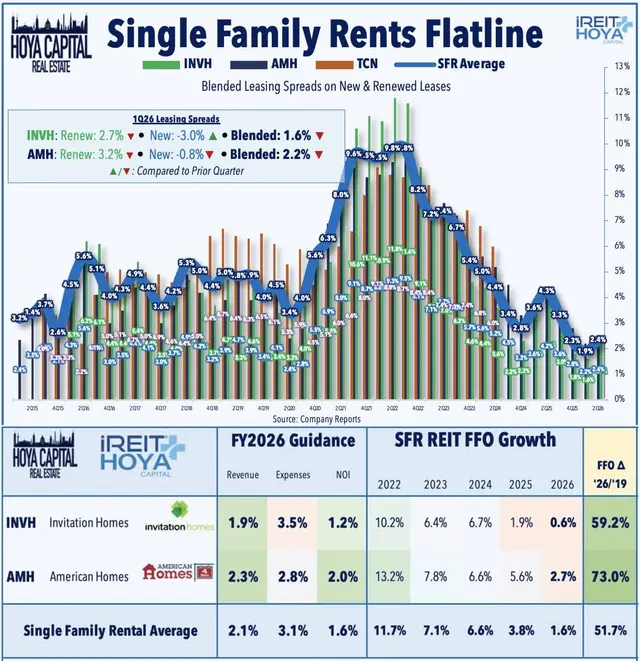

Winner #10: Single Family Rental: (Final Grade: B+)

Positives: Results were in line, with stable occupancy, improving April blended rent growth, and signs that pricing may be nearing a trough. INVH continued capital recycling, selling homes above implied public-market valuations while repurchasing stock and authorizing additional buybacks, reinforcing confidence in private-market asset values.

Negatives: New lease spreads remain negative, blended rent growth is near historical lows, and regulatory scrutiny around single-family rental ownership remains a persistent overhang. Sector sentiment remains tied to housing affordability, mortgage rates, and policy risk, even though operations remain stable and occupancy remains healthy.

Big Winners: Invitation Homes (INVH)

Earnings Recap: Better Results, Bigger Deals

REIT earnings results were considerably better than consensus expectations, with 58 REITs - or 59% of equity REITs providing full-year FFO guidance - raising their outlooks, well above the typical first-quarter raise rate of 40-45%, while just four REITs lowered guidance. The strongest upside came from Hotel, Senior Housing, Data Center, Billboard, Cold Storage, Net Lease, and Retail REITs, where guidance raises were supported by resilient demand, stronger leasing activity, pricing power, improving occupancy, and reaccelerating acquisition pipelines. Meanwhile, Residential REITs maintained guidance while reporting firmer April lease trends, suggesting that rent growth may be approaching a cyclical inflection as supply pressure begins to moderate. In Part 2 of our Earnings Recap later this week, we’ll take a closer look at the relative laggards of earnings season - including both outright disappointments and in-line performers that failed to generate enough upside to keep pace with the broader REIT rally. For now, the downside list was relatively contained, with weakness concentrated in Lab Space, mortgage REITs, Self-Storage, and Farmland. Meanwhile, M&A activity remained a defining theme of the season, as the private-market bid continued to put a valuation floor under discounted small- and mid-cap REITs while reinforcing the view that public-market pricing remains attractive for opportunistic real estate investors.

About the Author

David Auerbach boasts over two decades of experience in the securities industry, specializing as an institutional trader with a focus on Real Estate Investment Trusts (REITs), Equity and Preferred stocks, MLPs, ETFs, and Closed End Funds.

Based in Dallas, TX throughout his entire career, David currently serves as the Chief Investment Officer for Hoya Capital, managing the Hoya Housing 100 ETF (Ticker: HOMZ) and The High Yield Dividend ETF (Ticker: RIET). Previously, David held the position of Managing Director at Armada ETF Advisors, the sub-advisor for the Residential REIT ETF (Ticker: HAUS) and The Private Real Estate Strategy via Liquid REITs ETF (Ticker: PRVT).

Additionally, he acts as a consultant with IRRealized, LLC, focusing on corporate access in the REIT industry. David's industry journey includes roles at World Equity Group, Esposito Securities, and Green Street Advisors where he got his start in the REIT industry.

At Esposito Securities, he played a crucial role in building the REIT/Real Estate platform and worked extensively with institutional investors, Equity REITs, and ETF issuers.

Throughout his career, David has been quoted by reputable publications such as Bloomberg, WSJ, Financial Times, REIT.com, and GlobeSt.com. He has also made notable appearances as a featured guest on networks like Yahoo Finance, TD Ameritrade, and Bloomberg.

David holds a BBA in Finance from the University of Texas at Austin (May 1999) and an MBA in Finance from Southern Methodist University (May 2005). He maintains FINRA Series 7, 24, 55, and 63 registrations.

In his leisure time, David is an avid traveler, often found crisscrossing the country in pursuit of attending as many Phish concerts as possible.

Disclaimer

Please note this article is for information purposes only and does not in any way constitute investment advice. It is essential that you seek advice from a registered financial professional prior to making any investment decision.

Segments

See all

Mentioned ETFs

No specific ETFs were tagged

Further reading

Latest ETF News

See all ETF news

Advantages of ETFs over Mutual Funds1/6

Advantages of ETFs over Mutual Funds1/6

Lower Costs

In this guide, we'll explore the advantages of ETFs over mutual funds, giving you valuable insights into why ETFs have gained significant popularity among investors like yourself.

Leveraged ETFs: Unlocking the Potential for Amplified Returns1/6

Understanding Leveraged ETFs

Explore leveraged ETFs: potential for amplified returns & risks. 5 ETFs to consider across equities, commodities & fixed income.

What is a Leveraged ETF?1/6

Introducing Leveraged and Inverse ETFs

In this guide, we'll dive into the world of leveraged ETFs, exploring their definition, mechanics, potential risks, and rewards.

Recent educational content

ETF Trends

ETF Industry KPIs July 13, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

First Look ETF

First Look ETF: Cash Deployment, Bond, and Hedged ETFs

In this season 6 episode of First Look ETF, Stephanie Stanton examines the latest ETF marketplace trends with NYSE and guests.

ETF Trends

ETF Industry KPIs July 6, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

Asset TV

The ETF Show - The Evolution of Leveraged & Inverse ETFs

Leveraged and inverse ETFs have exploded in popularity over the past decade capturing more assets as retail traders seek to capture volatility.

Browse all educational columns

Build and Analyze Your ETF Portfolio Like a Pro

Create your own ETF portfolio in minutes and instantly see allocations, exposures, performance, and risk. Visualize diversification across asset classes, regions, and sectors. Stress-test ideas, compare benchmarks, and refine your strategy with professional-grade analytics.