Open Now: The Global ETF Survey Take the Survey →

Meet the Biggest Losers of REIT Earnings Season - Q1 2026

Even in a quarter where REITs broadly beat expectations, the real story was where the cracks refused to heal.

Keep up with what matters in ETFs

Get timely ETF insights, market trends, and top ideas straight to your inbox.

Your newsletter subscriptions with us are subject to ETF Central's Privacy Policy and Terms and Conditions.

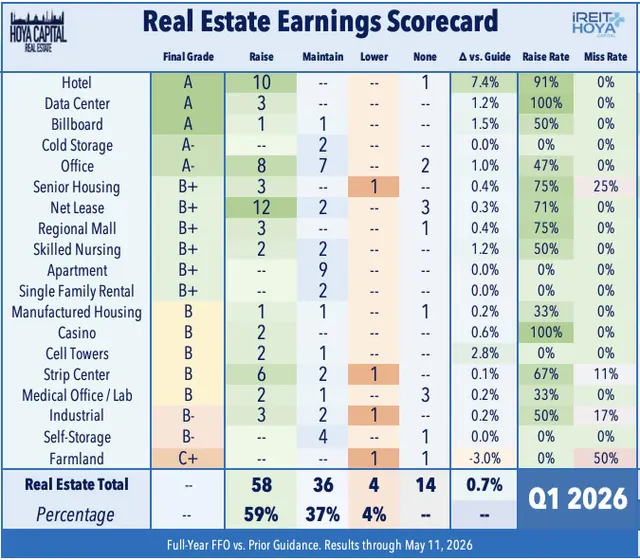

As noted Part 1, overall REIT earnings results were considerably better than consensus expectations and delivered a notably cleaner reporting period than several recent quarters, with fewer high-profile disappointments and a broader mix of upside surprises across sectors and market-cap tiers.

Of the 98 equity REITs that provided full-year FFO guidance, 58 REITs - or 59% - raised their outlooks, considerably above the typical first-quarter raise rate of roughly 40-45%, while 36 REITs - or 37% - maintained guidance, and just 4 REITs - or 4% - lowered guidance.

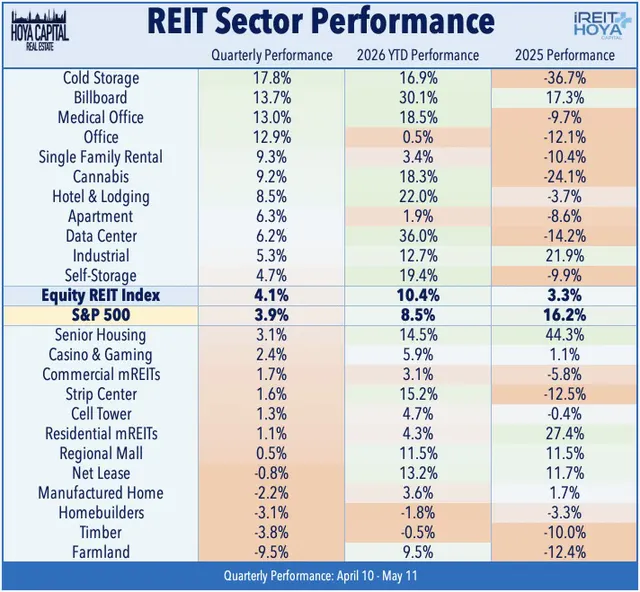

Since the start of earnings season, the Equity REIT Index is higher by 4.1%, outpacing the 3.9% gain from the S&P 500. While there were few outright bombshells, this earnings season produced a handful of laggards, with disappointments clustered in Lab Space, Commercial Mortgage, Residential Mortgage, Self-Storage, and Farmland REITs.

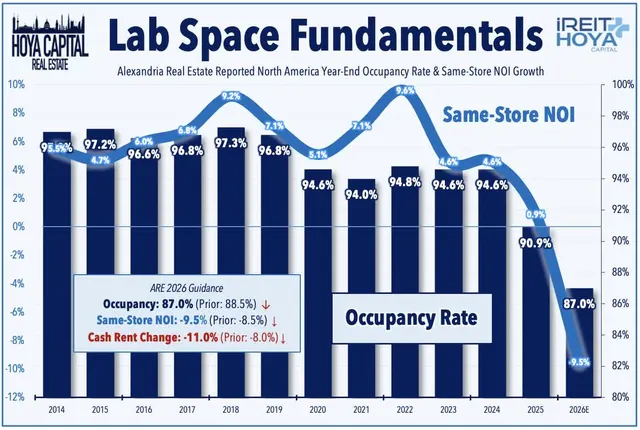

Lab Space remained the clearest downside standout, as Alexandria’s results reinforced a delayed recovery timeline, with soft leasing demand, declining occupancy, negative cash rent spreads, and another wave of expected 2027 move-outs pushing the earnings trough further into the future.

Commercial Mortgage REITs also remained under pressure, with credit stress still concentrated in multifamily bridge loans, office exposure, and impaired transitional loans, prompting continued book value erosion, elevated credit-loss provisions, and another dividend reset from Arbor.

Residential Mortgage REITs were broadly in line from an earnings-coverage perspective, but book values were pressured across rate-sensitive portfolios amid elevated interest-rate volatility.

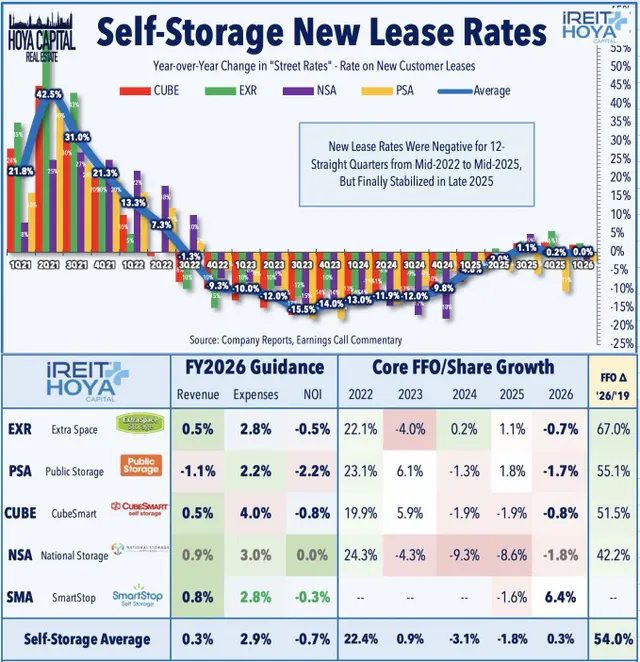

Self-Storage REITs showed tentative signs of stabilization entering peak leasing season, with move-in rent declines moderating and occupancy trends improving, but move-in rents and in-place rents remain soft, and a fuller recovery still depends on improved housing turnover.

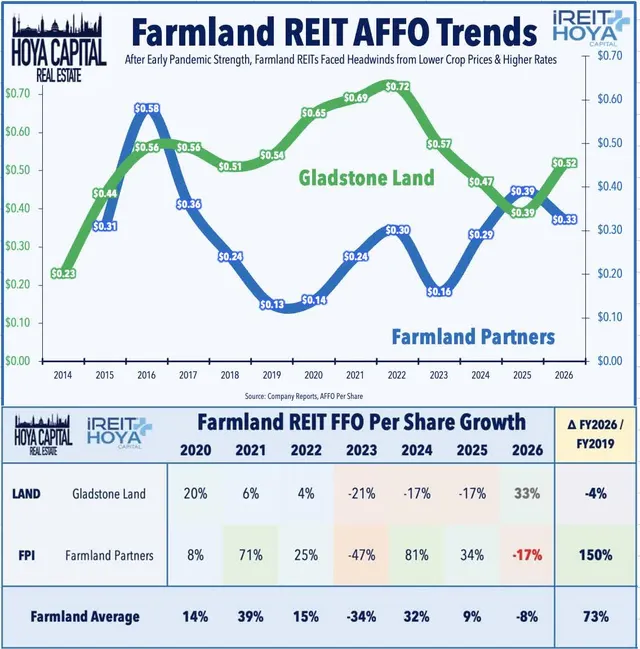

Farmland REITs were also weaker than expected, led by Farmland Partners’ sharp guidance reduction tied to higher borrower-specific credit-loss provisioning, while Gladstone Land continues to face tenant-payment issues.

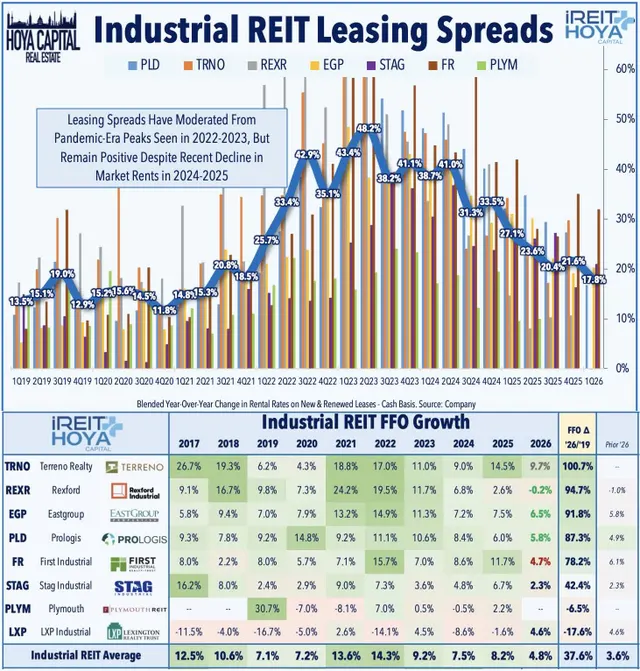

Several other property sectors landed closer to the “in-line” bucket rather than the outright loser category. Industrial REITs delivered steady results, supported by strong leasing spreads and high occupancy, but Southern California weakness, slowing same-store NOI growth, and maintained - rather than raised - guidance kept the group from joining the upside leaders.

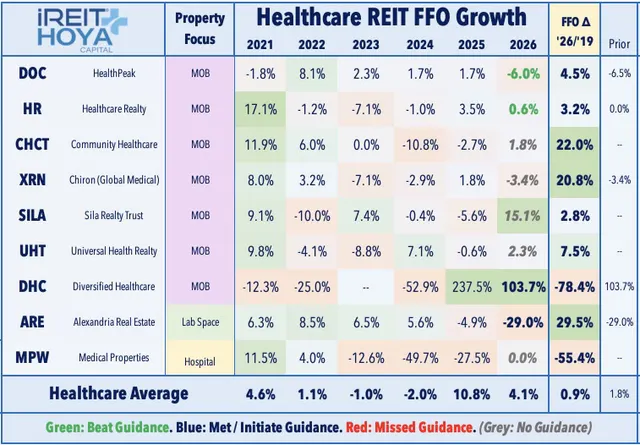

Medical Office REITs were generally constructive, with improving leasing, occupancy, and tenant-retention trends, but smaller platforms remain uneven, and lingering portfolio-transition and capital-allocation questions kept the group in the steady-but-unspectacular bucket.

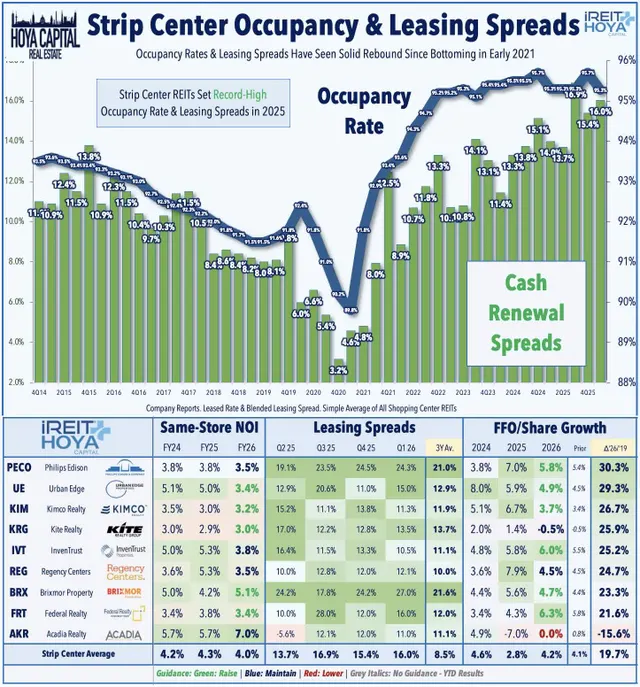

Strip Center REITs posted another solid quarter, supported by healthy occupancy, signed-not-open pipelines, and strong cash leasing spreads, though expectations were already elevated after a strong multi-year run.

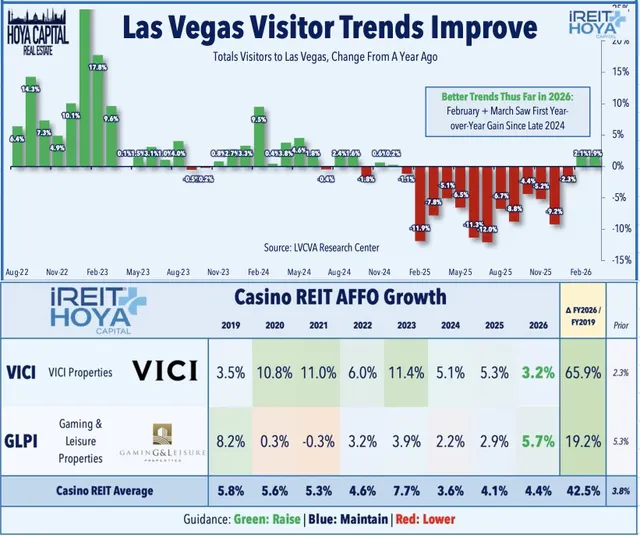

Casino REITs remained dependable, with steady rent coverage and attractive external-growth opportunities, but tenant credit concerns and higher capital costs limited enthusiasm.

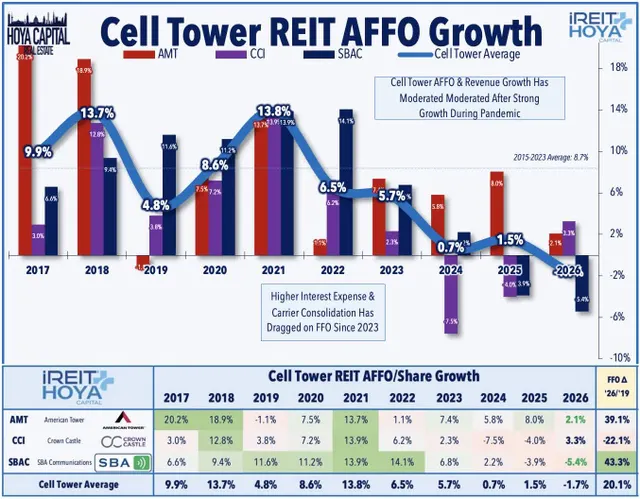

Cell Tower REITs showed stabilization, modest guidance raises, and renewed strategic interest, but domestic leasing remains below prior 5G-cycle levels.

Manufactured Housing REITs continued to benefit from high occupancy and limited supply, though RV, marina, and UK exposure added macro sensitivity. Cannabis REITs showed progress on tenant resolutions and re-leasing, but credit risk remains highly tenant-specific. Among individual names, three REITs posted double-digit declines: Franklin Street (FSP), National Health Investors (NHI), and Farmland Partners (FPI) - a notably short list of major losers compared with the broad-based upside across the sector.

![]()

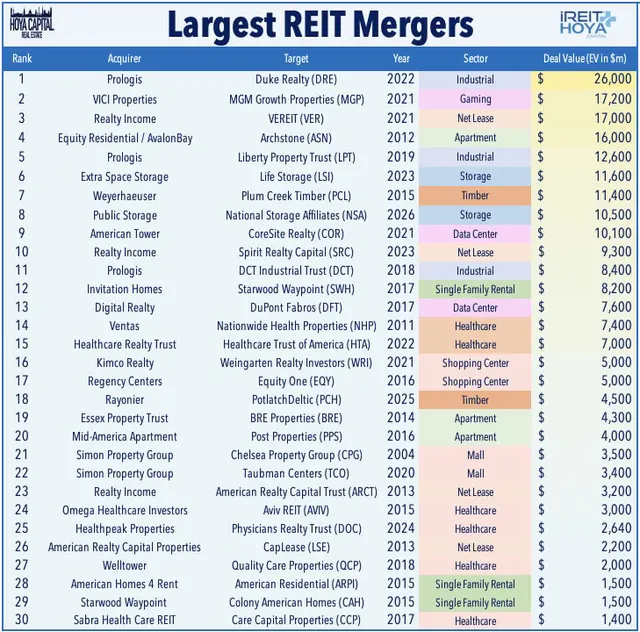

M&A news again stole some of the thunder from earnings season, reinforcing the ongoing “REIT Exodus” theme that has persisted over the past several quarters - but the capital markets story is no longer purely one-way.

Modiv Industrial (MDV) surged after Global Net Lease (GNL) announced an all-stock acquisition of the single-tenant industrial REIT in a deal valued at roughly $550M, continuing the push toward consolidation among smaller-cap platforms that have struggled to earn an efficient public-market cost of capital. In healthcare, SILA Realty (SILA) agreed to be acquired by Blue Owl in a $2.4B private-equity takeout, providing another validation point for private-market healthcare real estate values. Back in March, Whitestone REIT (WSR) agreed to be acquired by Ares Management in a $1.7B deal, while SBA Communications (SBAC) is reportedly exploring a potential sale, putting a roughly $34B cell tower platform into play. Adding to the M&A buzz, reports of early-stage discussions between AvalonBay (AVB) and Equity Residential (EQR) point to the possibility of a mega-merger that could reshape the U.S. apartment REIT landscape.

At the same time, the IPO window has shown signs of reopening after a multi-year drought. Taken together, the recent deal flow reinforces a central REIT theme: strategic buyers continue to step in where public markets have been slow to fully value real estate platforms, while the reopening IPO pipeline suggests that the public market is not closed - just more selective.

For public REIT investors, that private-market bid is increasingly relevant not just as a source of takeout premiums, but as a valuation anchor for discounted REITs with durable cash flows, high-quality assets, and credible paths to balance-sheet repair or external growth.

The ETF Industry Is Evolving Fast

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.

Losers of REIT Earnings Season

Loser #1: Farmland: (Final Grade: C+)

Negatives: FPI lowered its 2026 FFO outlook sharply, now expecting a -17% decline versus its prior outlook for a -10% decline, driven by higher credit-loss provisioning tied to borrower-specific risk within its loan program. LAND still faces tenant payment issues, vacant farms, participation-rent uncertainty, and crop/weather/water volatility, while both names remain sensitive to rates, agricultural commodity pricing, and liquidity constraints.

Positives: Farmland REIT results showed some stabilization beneath the surface, with LAND benefiting from stronger pistachio and almond pricing, early pistachio bonus revenue, improving crop-share economics, and continued investment in water security.

Big Winners: None

Big Losers: Farmland Partners (FPI)

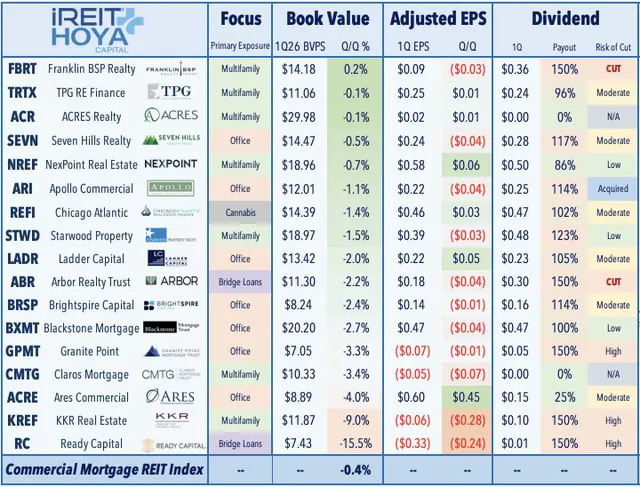

Loser #2: Commercial Mortgage REITs (Final Grade: C+)

Negatives: Credit stress remains concentrated in multifamily bridge lending, office exposure, and impaired transitional loans. ABR cut its dividend again, RC posted a large book-value decline, and CMTG/ACRE saw further negative credit migration. Tighter refinancing markets, slower lease-up, elevated rates, and limited transaction liquidity remain the dominant overhangs, keeping dividend coverage and book-value stability under pressure.

Positives: Some smaller lenders showed stabilization, with flat or modest book-value declines, performing loan books, improving risk ratings, and adequate dividend coverage. Several managers generated liquidity through loan sales, liquidations, and resolutions, while select platforms benefited from signs of multifamily stabilization and improving borrower-level fundamentals.

Big Winners: NexPoint Real Estate (NREF), ACRES Realty (ACR)

Big Losers: Arbor Realty (ABR), Granite Point (GPMT)

Loser #3: Lab Space (Final Grade: C+)

Negatives: Alexandria's results reinforced a delayed trough, with leasing volume at the lowest level since 2016, occupancy down sharply, cash leasing spreads deeply negative, and same-store NOI under pressure. Expected 2027 move-outs, extended downtime, weaker tenant expansion activity, and elevated development deliveries pushed the recovery timeline further out, keeping lab space among the clearest laggards.

Positives: Development lease-up showed some progress, and management expects leasing activity to rebound in the near term. Healthpeak’s more constructive life science commentary suggested conditions may be less severe for diversified platforms, while long-term demand drivers remain intact if biotech funding, tenant confidence, and capital availability recover, particularly across well-located research clusters with stronger institutional tenant bases.

Loser #4: Self-Storage REITs: (Final Grade: B-)

Negatives: Recovery remains slow and dependent on housing turnover, which has not yet meaningfully recovered. Move-in rates remain muted, in-place rents remain under pressure, all four REITs maintained guidance for same-store NOI declines, and the group still lacks a clear catalyst for a full pricing recovery beyond gradual seasonal improvement.

Positives: Tentative stabilization emerged entering peak leasing season, with move-in rent declines moderating sharply at PSA, occupancy and churn trends improving, and CUBE/EXR maintaining guidance with generally better same-store results. Limited new investment activity and slowing supply growth may help rebalance the sector over time.

Big Winners: National Storage (NSA)

Big Losers: SmartStop (SMA)

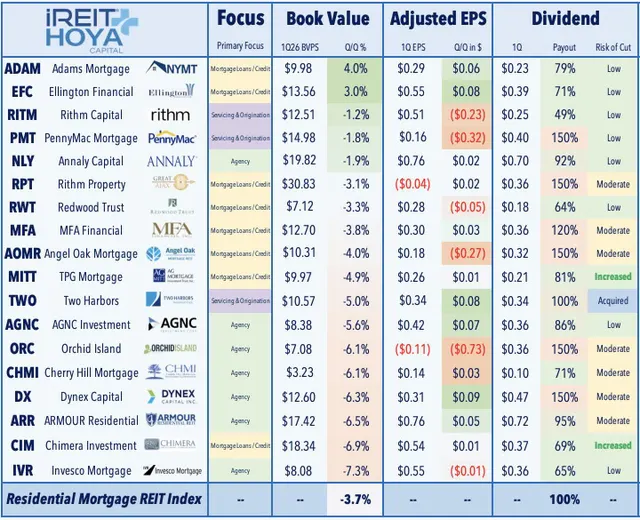

Loser #5: Residential Mortgage REITs (Final Grade: B-)

Negatives: Book values were pressured across agency- and rate-sensitive portfolios, with several names reporting mid-single-digit BVPS declines. PMT’s run-rate earnings outlook fell below its dividend, while elevated rate volatility continues to pressure spreads, hedging outcomes, leverage decisions, and investor confidence across the residential mortgage REIT group, particularly for portfolios more exposed to duration risk and prepayment uncertainty.

Positives: Results were broadly in line, with no major credit or liquidity issues despite higher interest-rate volatility during the quarter. Earnings coverage remained adequate across many names, several platforms highlighted opportunities to deploy capital into dislocations, and select names posted book-value growth or dividend coverage that exceeded expectations, suggesting the pressure was manageable rather than a broader sector stress event.

Big Winners: Adams Mortgage (ADAM), Two Harbors (TWO)

Big Losers: Redwood (RWT), PennyMac (PMT)

Loser #6 Industrial: (Final Grade: B-)

Negatives: Southern California remains soft, with REXR posting negative cash spreads and declining market rents. Several names maintained rather than raised guidance, while occupancy drift, tariff uncertainty, larger-user caution, and slowing same-store NOI growth kept the group in the status-quo bucket despite improving national demand signals and early signs of supply pressure easing. FR also lowered guidance, reflecting costs tied to its proxy fight.

Positives: Industrial results were broadly in line, supported by strong cash leasing spreads, high occupancy, solid renewal activity, and emerging data-center-adjacent and manufacturing demand. Sunbelt and smaller-bay logistics markets remain healthier, while development pipelines continue to normalize after peak supply and long-term embedded mark-to-market upside remains meaningful across many portfolios.

Big Winners: Rexford (REXR), Industrial Logistics (ILPT)

Big Losers: None

Steady Performers This Earnings Season

Medical Office: (Final Grade: B)

Positives: Medical office joined the positive healthcare trend, with HR and DOC showing better leasing, occupancy, and NOI momentum. Sila Realty’s acquisition by Blue Owl provided another validation point for private-market healthcare real estate values, while DOC’s guidance raise and constructive life science commentary eased investor concerns. HR also delivered strong tenant retention, leasing spreads, occupancy gains, and share repurchases.

Negatives: Smaller MOB peers remain more mixed, with occupancy pressure, portfolio transitions, and capital allocation questions still weighing on results. Hospital exposure remains risky in select names, DOC still has lab weakness, and XRN’s pivot to SHOP brought guidance withdrawal, a dividend cut, near-term dilution, and execution risk.

Big Winners: Healthpeak (DOC), Sila Realty (SILA)

Big Losers: Chiron / Global Medical (XRN), Universal Health Realty (UHT)

Strip Centers: (Final Grade: B)

Positives: Another solid quarter, with six of nine names raising FFO guidance and cash leasing spreads averaging mid-teens. Occupancy remains healthy, signed-not-open pipelines support future growth, and tight open-air retail supply continues to favor grocery-anchored, mixed-use, and high-income trade-area portfolios with durable tenant demand.

Negatives: Occupancy has modestly normalized from early-2025 peaks, and several stocks declined despite guidance raises, suggesting expectations are already elevated. AKR trimmed FFO guidance, rent-spread strength may moderate from exceptional levels, and consumer bifurcation could pressure weaker tenants or lower-income trade areas if spending slows.

Big Winners: Federal Realty (FRT)

Big Losers: InvenTrust (IVT)

Casino: (Final Grade: B)

Positives: Casino REITs delivered steady external growth and attractive deal spreads, with GLPI raising AFFO guidance, completing sizable acquisitions at roughly 8% cap rates, and highlighting a robust development pipeline. Regional gaming trends appear to be stabilizing after a softer 2025, supporting steady rent coverage and transaction activity.

Negatives: Tenant credit markets remain uneven, and operator turbulence can cut both ways by creating investment opportunities but also raising risk premiums. Growth depends on continued acquisition and development execution, while regional gaming demand remains economically sensitive and elevated rates keep capital allocation and tenant balance sheets in focus.

Big Winner: None

Big Loser: None

Cell Tower: (Final Grade: B)

Positives: Results were steady, with modest guidance raises, a stabilizing domestic leasing backdrop, and renewed strategic interest following reports that SBAC is exploring a potential sale. AMT de-risked guidance by removing DISH exposure and showed CoreSite data center momentum, while SBAC maintained discipline around deleveraging and investment-grade rating objectives as carrier activity gradually shifts toward densification.

Negatives: U.S. carrier activity remains uneven, with densification and capacity upgrades slower than prior 5G deployment cycles. SBAC still expects FFO declines, DISH-related churn and international complexity remain overhangs, and the group’s growth profile remains more modest than in prior tower cycles despite stabilization.

Big Winners: Crown Castle (CCI)

Big Losers: None

Manufactured Housing: (Final Grade: B)

Positives: Core manufactured housing fundamentals remained steady, with high occupancy, limited new supply, and persistent affordable housing demand. SUI raised FFO and NOI guidance, while UMH delivered solid same-property NOI growth, improving occupancy, and better rental-home utilization, supporting expectations for stronger seasonal growth ahead.

Negatives: RV and UK segments remain macro-sensitive and continue to dilute the cleaner manufactured housing story. SUI struck a cautious tone on fuel costs, discretionary spending, and summer travel, while UMH faced weather, expense, and interest-cost headwinds despite stable underlying demand and improving occupancy trends.

Big Winner: None

Big Loser: None

Cannabis: (Final Grade: B)

Positives: Cannabis REITs showed signs of stabilization after a difficult stretch, with IIPR delivering steady results, resolving several tenant issues, leasing former troubled assets, and highlighting potential tenant credit improvement from Schedule III reclassification and 280E tax relief for medical operators. Investors finally saw a credible path toward a healthier cycle.

Negatives: Tenant credit issues have not disappeared, and the regulatory timeline around Schedule III and adult-use treatment remains uncertain. The sector remains highly concentrated, small, and tenant-specific, while AFFO is still down year-over-year, and investor confidence depends on continued rent collections, leasing progress, and further legal clarity.

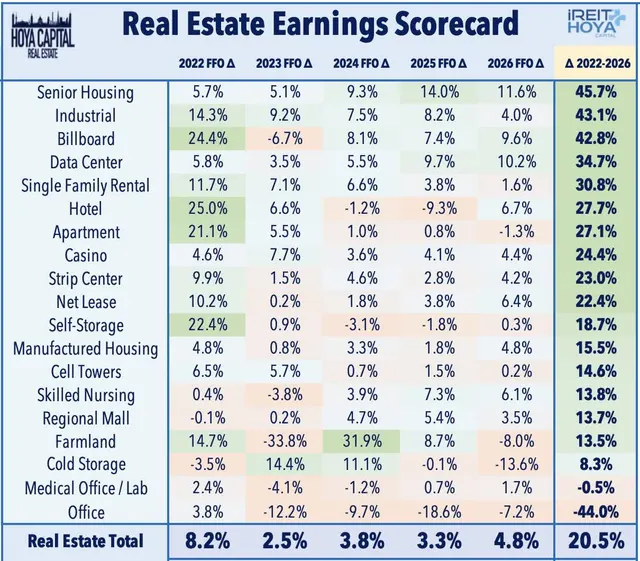

Earnings Recap: Better Results, Bigger Deals

REIT earnings results were considerably better than consensus expectations, with 58 REITs - or 59% of equity REITs providing full-year FFO guidance - raising their outlooks, well above the typical first-quarter raise rate of 40-45%, while just four REITs lowered guidance.

But Part 2 of our Earnings Recap focuses on the other side of the ledger: the relative laggards and in-line performers that failed to match the broader upside across the sector.

The downside list was relatively contained, with weakness concentrated in Lab Space, Commercial Mortgage, Residential Mortgage, Self-Storage, Farmland, and select Office REITs, where delayed demand recoveries, book-value pressure, credit-loss provisions, weak move-in rents, and refinancing constraints remained key headwinds.

Lab Space remained the clearest disappointment, as Alexandria’s results pushed the expected recovery timeline further out, while mortgage REITs continued to face pressure from elevated rate volatility, credit migration, and tighter capital markets.

Self-Storage showed tentative signs of stabilization, but still lacked a clear catalyst beyond gradual seasonal improvement, while Farmland results were weighed down by borrower-specific credit issues and tenant payment uncertainty.

Several other sectors - including Industrial, Medical Office, Strip Centers, Casino, Cell Tower, Manufactured Housing, and Cannabis - were steadier but unspectacular, generally delivering stable fundamentals without enough upside surprise to join the earnings-season winners.

Meanwhile, M&A remained a defining theme, as private-market bids and strategic interest continued to put a valuation floor under discounted REITs and reinforced the view that public-market pricing remains attractive for opportunistic real estate investors.

About the Author

David Auerbach boasts over two decades of experience in the securities industry, specializing as an institutional trader with a focus on Real Estate Investment Trusts (REITs), Equity and Preferred stocks, MLPs, ETFs, and Closed End Funds.

Based in Dallas, TX throughout his entire career, David currently serves as the Chief Investment Officer for Hoya Capital, managing the Hoya Housing 100 ETF (Ticker: HOMZ) and The High Yield Dividend ETF (Ticker: RIET). Previously, David held the position of Managing Director at Armada ETF Advisors, the sub-advisor for the Residential REIT ETF (Ticker: HAUS) and The Private Real Estate Strategy via Liquid REITs ETF (Ticker: PRVT).

Additionally, he acts as a consultant with IRRealized, LLC, focusing on corporate access in the REIT industry. David's industry journey includes roles at World Equity Group, Esposito Securities, and Green Street Advisors where he got his start in the REIT industry.

At Esposito Securities, he played a crucial role in building the REIT/Real Estate platform and worked extensively with institutional investors, Equity REITs, and ETF issuers.

Throughout his career, David has been quoted by reputable publications such as Bloomberg, WSJ, Financial Times, REIT.com, and GlobeSt.com. He has also made notable appearances as a featured guest on networks like Yahoo Finance, TD Ameritrade, and Bloomberg.

David holds a BBA in Finance from the University of Texas at Austin (May 1999) and an MBA in Finance from Southern Methodist University (May 2005). He maintains FINRA Series 7, 24, 55, and 63 registrations.

In his leisure time, David is an avid traveler, often found crisscrossing the country in pursuit of attending as many Phish concerts as possible.

Disclaimer

Please note this article is for information purposes only and does not in any way constitute investment advice. It is essential that you seek advice from a registered financial professional prior to making any investment decision.

Segments

See all

Mentioned ETFs

No specific ETFs were tagged

Further reading

Latest ETF News

See all ETF news

Advantages of ETFs over Mutual Funds1/6

Advantages of ETFs over Mutual Funds1/6

Lower Costs

In this guide, we'll explore the advantages of ETFs over mutual funds, giving you valuable insights into why ETFs have gained significant popularity among investors like yourself.

Leveraged ETFs: Unlocking the Potential for Amplified Returns1/6

Understanding Leveraged ETFs

Explore leveraged ETFs: potential for amplified returns & risks. 5 ETFs to consider across equities, commodities & fixed income.

What is a Leveraged ETF?1/6

Introducing Leveraged and Inverse ETFs

In this guide, we'll dive into the world of leveraged ETFs, exploring their definition, mechanics, potential risks, and rewards.

Recent educational content

ETF Trends

ETF Industry KPIs July 13, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

First Look ETF

First Look ETF: Cash Deployment, Bond, and Hedged ETFs

In this season 6 episode of First Look ETF, Stephanie Stanton examines the latest ETF marketplace trends with NYSE and guests.

ETF Trends

ETF Industry KPIs July 6, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

Asset TV

The ETF Show - The Evolution of Leveraged & Inverse ETFs

Leveraged and inverse ETFs have exploded in popularity over the past decade capturing more assets as retail traders seek to capture volatility.

Browse all educational columns

The ETF Industry Is Evolving Fast

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.