Open Now: The Global ETF Survey Take the Survey →

Is U.S. Cannabis Finally Becoming Investable?

Rescheduling alters operating economics in a historically constrained sector.

Keep up with what matters in ETFs

Get timely ETF insights, market trends, and top ideas straight to your inbox.

Your newsletter subscriptions with us are subject to ETF Central's Privacy Policy and Terms and Conditions.

President Trump signed an executive order on December 18th, directing the rescheduling of cannabis to Schedule III under the Controlled Substances Act. The decision marks the most significant federal shift in U.S. cannabis policy in more than 50 years and formally recognizes accepted medical use while removing cannabis from the same classification as heroin and cocaine.

While the order does not legalize cannabis at the federal level, it represents a structural change that materially alters operating economics, regulatory treatment, and the long-term investment framework for the U.S. cannabis industry.

Like what you're reading?

Stay in the loop — get the latest ETF insights: trends, analysis, and expert picks.

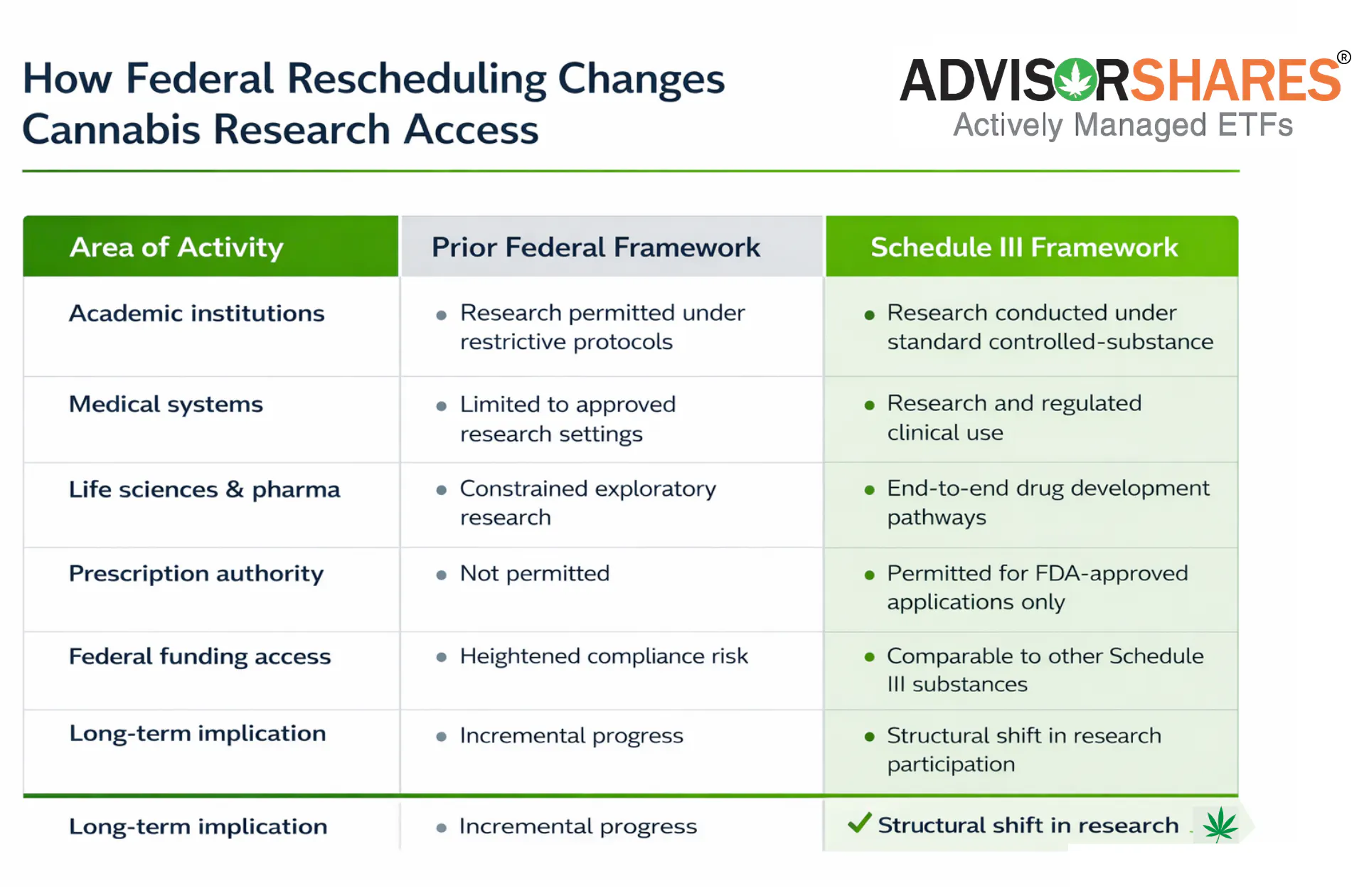

Research Access and Medical Validation

Under Schedule I, research involving cannabis has required special federal approvals, limited sourcing options, and extensive administrative hurdles. These constraints have historically slowed clinical research and discouraged participation from universities, hospitals, and private research organizations.

Schedule III status does not eliminate regulatory oversight, but it meaningfully reduces research friction by:

- Expanding the number of institutions eligible to conduct federally compliant research

- Simplifying approval processes for clinical trials and academic studies

- Improving access to standardized research-grade cannabis inputs

- Encouraging greater participation from pharmaceutical, biotech, and medical research entities

Over time, expanded research may improve data quality around medical efficacy, dosing, and safety supporting more informed regulatory, healthcare, and policy decisions. While outcomes are not guaranteed, the shift lowers barriers to evidence generation that were unique to Schedule I classification.

Medicare Coverage and CBD-Based Therapies

Federal officials announced that Medicare is expected to begin covering certain cannabis-derived therapies as early as April, marking a significant shift in how these products are treated within federal healthcare programs.

Coverage would apply only to approved, regulated products, and implementation will depend on additional clinical data, standardized product testing, and ongoing regulatory review.

While this does not represent blanket coverage of cannabis or over-the-counter CBD products, the announcement signals a meaningful change in policy direction, bringing cannabis-derived treatments into a formal evaluation framework alongside other regulated therapies.

The requirement for further data and testing underscores that access will expand through medical and regulatory channels, rather than through broad legalization.

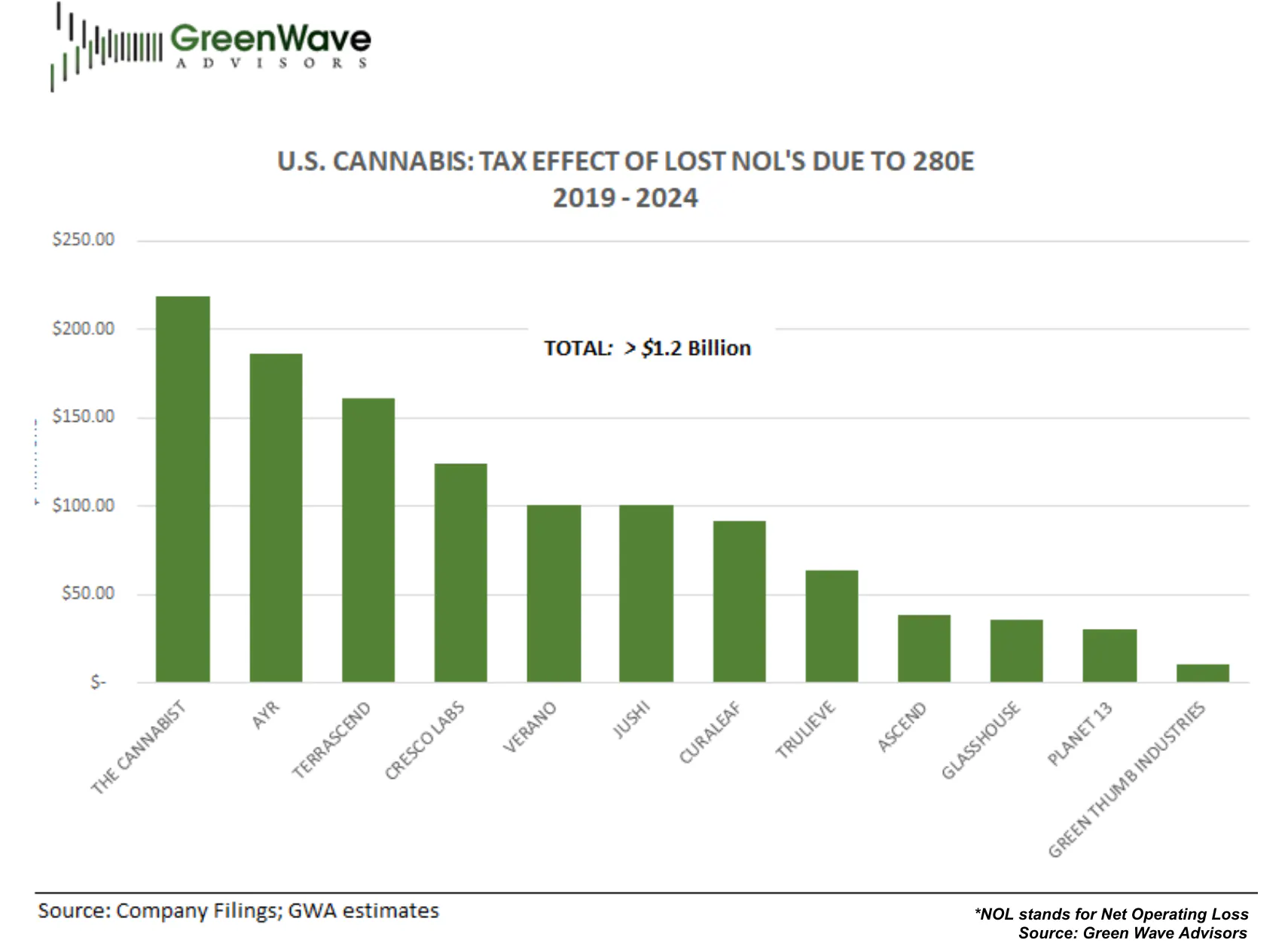

The Immediate Economic Impact of Rescheduling

One of the most consequential outcomes of Schedule III status is the effective removal of IRS Section 280E for state-legal cannabis operators.

Section 280E has historically prevented cannabis businesses from deducting ordinary operating expenses, forcing them to pay taxes on gross profit rather than net income. With rescheduling now in place, those restrictions no longer apply.

- Ordinary business deductions are allowed

- Effective tax rates move toward standard corporate levels

- Industry-wide tax savings are estimated at approximately $1.2 billion annually

- Cash flow improves without requiring revenue growth or geographic expansion

Rescheduling alters operating economics in a historically constrained sector, allowing profitability to improve through cost normalization rather than increased demand assumptions.

Why This Matters for Investors

Cash Flow Improves Without Growth Assumptions

Unlike many thematic investment narratives that depend on long-term demand acceleration, the benefits of rescheduling are driven by changes to cost structure. This reduces survival risk and improves earnings quality across the industry.

Capital Access Shifts From Prohibited to Evaluated

Schedule I classification functioned as a hard exclusion for many banks, custodians, and institutional allocators. With that designation removed, exposure can now be evaluated, structured, and monitored within traditional risk frameworks rather than categorically excluded.

Cannabis Re-Enters the Investable Conversation

Cannabis has long been visible but difficult to allocate to at scale. Rescheduling reframes the sector as one undergoing regulatory normalization rather than one operating permanently outside federal acceptance.

What Schedule III Changes and What Remains Conditional

Schedule III is a major federal signal, but it does not automatically resolve every structural constraint in cannabis.

The clearest near-term effects are tied to tax treatment and operating economics, while other market-structure improvements remain conditional on follow-on policy actions, regulatory guidance, and institutional adoption.

Legislative efforts such as the SAFER Banking Act remain central to expanding access to traditional financial services for businesses operating legally under state law.

If advanced, banking reform could:

Provide clearer legal protections for federally regulated financial institutions serving cannabis-related clients

- Reduce reliance on cash-based operations, lowering operational and security risk

- Expand access to basic banking functions such as deposits, payroll, lending, and treasury services

- Incorporate updated consumer and depositor safeguards reflected in recent legislative proposals

Exchange Eligibility Over Time

Rescheduling alone does not confer eligibility for listing on major U.S. exchanges, such as the NYSE or Nasdaq. However, removing cannabis from Schedule I may reduce a key regulatory obstacle over the longer term.

Potential implications include:

- A broader potential investor audience as listing constraints evolve

- Improved liquidity and transparency if additional regulatory requirements are met

Any such changes would depend on exchange rules, issuer qualifications, and further federal guidance.

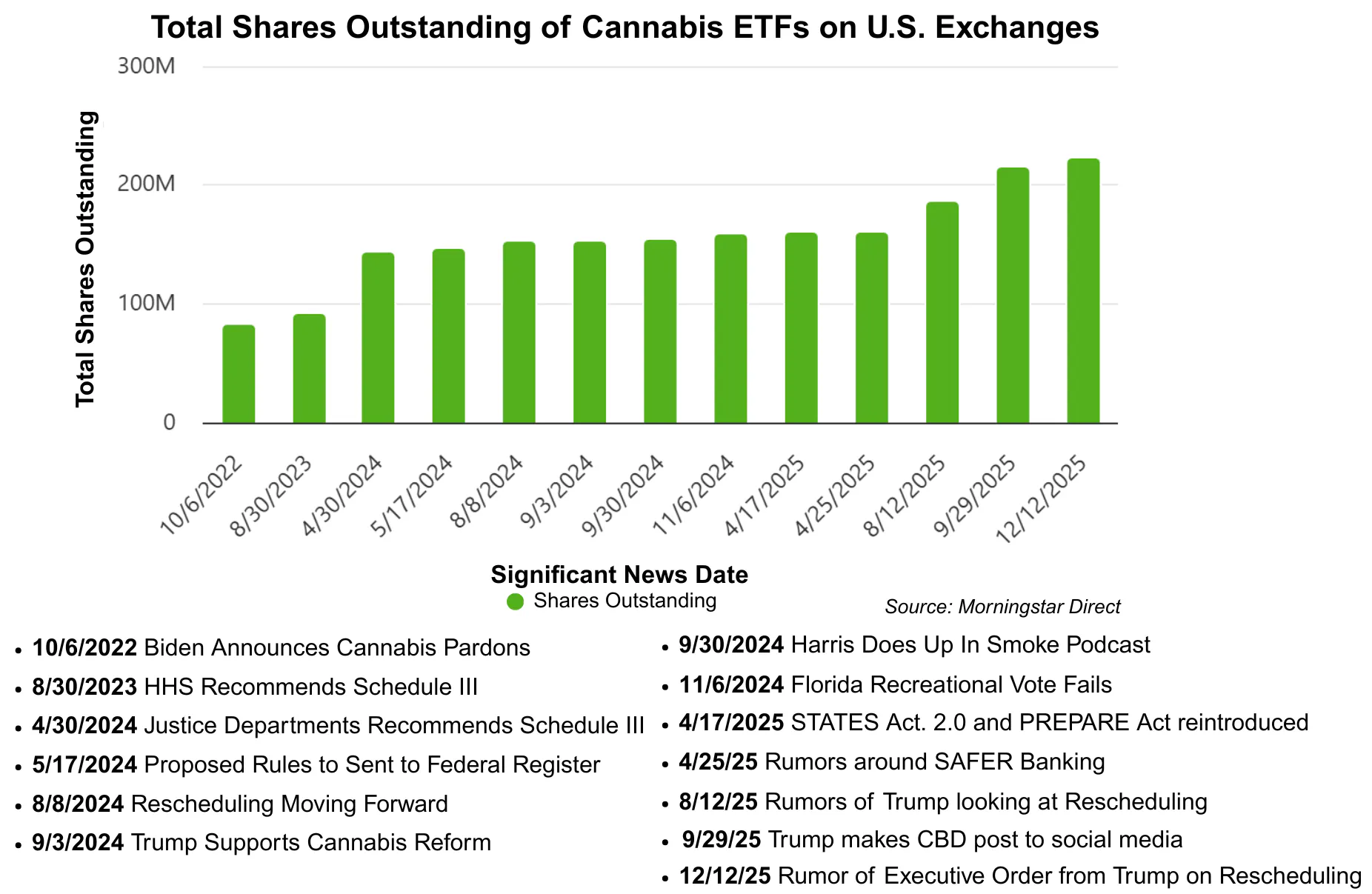

Why ETFs Matter in a Post-Rescheduling Environment

As cannabis transitions from regulatory exception to regulatory normalization, exchange-traded funds play a central role in how investors access the theme.

ETFs offer:

Diversification across operators and subsectors, reducing single-company risk

- Liquidity and transparency, important in a policy-driven and volatile market

- Operational simplicity, eliminating custody, listing, and security-specific complexity

- Portfolio flexibility, allowing exposure to be sized, rebalanced, and risk-managed

In sectors shaped by regulation and evolving market structure, ETFs provide a practical way to participate without relying on individual company outcomes.

Cannabis remains volatile and policy-sensitive, but the investment framework has shifted. With Schedule III in place, operating economics improve, capital access becomes more feasible, and regulatory uncertainty begins to narrow.

For investors evaluating thematic exposure, the post-rescheduling environment highlights why ETFs are often used to navigate complex, transitioning industries offering diversified, transparent access as the U.S. cannabis market enters its next chapter.

The opinions expressed in this publication are those of the authors and are subject to change. They do not purport to reflect the opinions or views of ETF Central or its members. ETF central does not guarantee the accuracy, completeness, or reliability of the information provided.

Sources:

- Herring Bank. Safe Banking Act & Cannabis Banking. June 2025.

- Accountants & Advisors. Financial Institution Internal Controls, Risk Management Impacted by Possible Federal Legislation for Cannabis Businesses. April 2025.

- GreenWave Advisors. The GreenWave Buzz. How Much Longer will the Snake (280E) remain in the “Grass”? September 2025.

- Morningstar Direct

The opinions expressed in this publication are those of the authors and are subject to change. They do not purport to reflect the opinions or views of ETF Central or its members. ETF Central does not guarantee the accuracy, completeness, or reliability of the information provided.

Latest ETF News

See all ETF news

Advantages of ETFs over Mutual Funds1/6

Advantages of ETFs over Mutual Funds1/6

Lower Costs

In this guide, we'll explore the advantages of ETFs over mutual funds, giving you valuable insights into why ETFs have gained significant popularity among investors like yourself.

Leveraged ETFs: Unlocking the Potential for Amplified Returns1/6

Understanding Leveraged ETFs

Explore leveraged ETFs: potential for amplified returns & risks. 5 ETFs to consider across equities, commodities & fixed income.

What is a Leveraged ETF?1/6

Introducing Leveraged and Inverse ETFs

In this guide, we'll dive into the world of leveraged ETFs, exploring their definition, mechanics, potential risks, and rewards.

Recent educational content

ETF Trends

ETF Industry KPIs July 6, 2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape.

Asset TV

The ETF Show - The Evolution of Leveraged & Inverse ETFs

Leveraged and inverse ETFs have exploded in popularity over the past decade capturing more assets as retail traders seek to capture volatility.

Asset TV

The ETF Show - Investors Turn to Small Caps as Value Outperforms

After years of outflows, small caps have attracted interest as the Russell 2000 outperforms the broad market. Chris Parker, Senior Portfolio Manager from Thrivent Asset Management joins the ETF Show to discuss.

ETF Trends

ETF Industry KPIs 6/29/2026

This week’s KPI data overview highlights key metrics and trends shaping the ETF landscape:

Browse all educational columns

Build and Analyze Your ETF Portfolio Like a Pro

Create your own ETF portfolio in minutes and instantly see allocations, exposures, performance, and risk. Visualize diversification across asset classes, regions, and sectors. Stress-test ideas, compare benchmarks, and refine your strategy with professional-grade analytics.